Vishay Intertechnology has had an impressive run over the past six months. While the S&P 500 has been flat, the stock has returned 9.5% and now trades at $16.66. This performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Vishay Intertechnology, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think Vishay Intertechnology Will Underperform?

We’re glad investors have benefited from the price increase, but we don't have much confidence in Vishay Intertechnology. Here are three reasons you should be careful with VSH and a stock we'd rather own.

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Vishay Intertechnology’s 4.2% annualized revenue growth over the last five years was mediocre. This was below our standard for the semiconductor sector. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

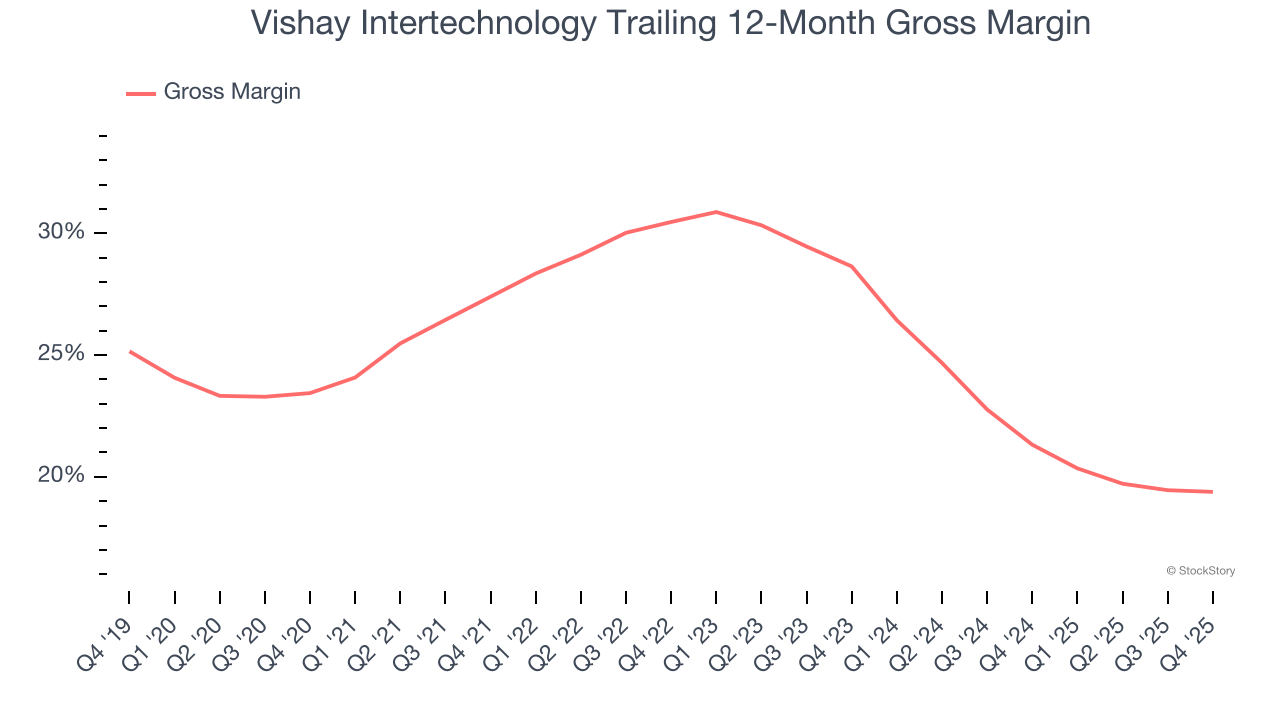

2. Low Gross Margin Reveals Weak Structural Profitability

Gross profit margin is a key metric to track because it shows how much money a semiconductor company gets to keep after paying for its raw materials, manufacturing, and other input costs.

Vishay Intertechnology’s gross margin is one of the worst in the semiconductor industry, signaling it operates in a competitive market and lacks pricing power. As you can see below, it averaged a 20.3% gross margin over the last two years. Said differently, Vishay Intertechnology had to pay a chunky $79.67 to its suppliers for every $100 in revenue.

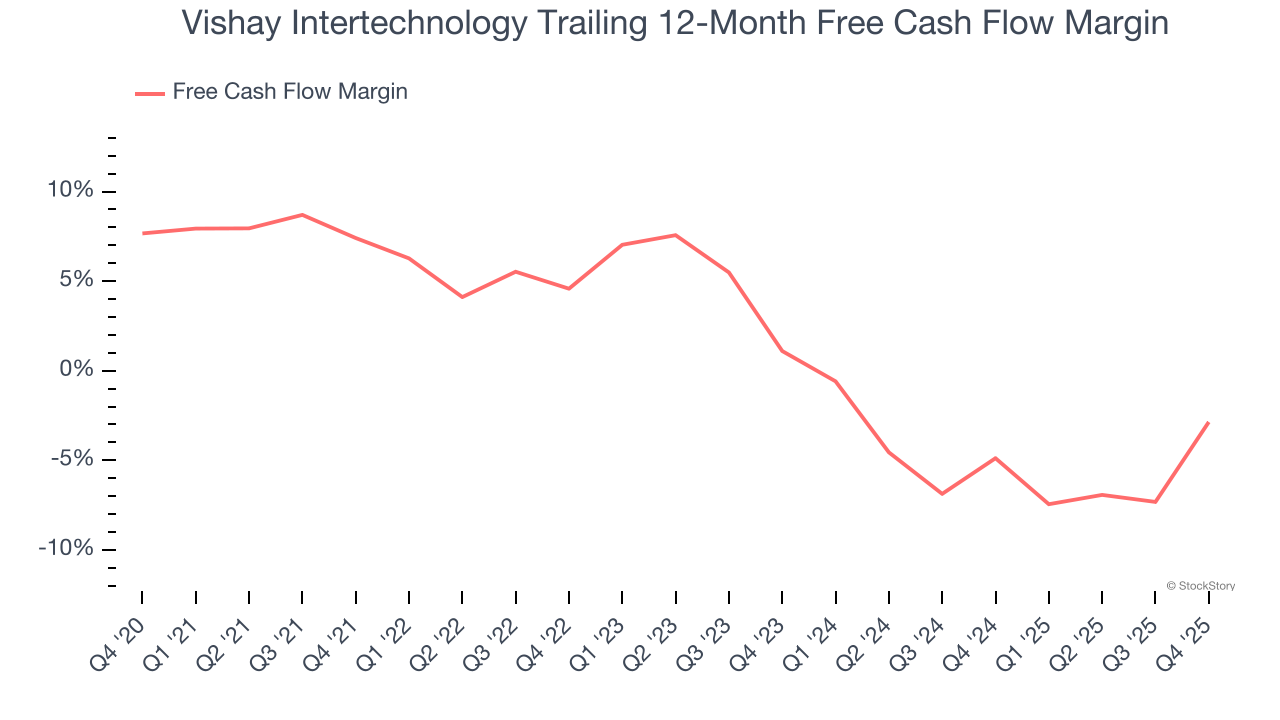

3. Cash Burn Ignites Concerns

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While Vishay Intertechnology posted positive free cash flow this quarter, the broader story hasn’t been so clean. Vishay Intertechnology’s demanding reinvestments have drained its resources over the last two years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 3.8%, meaning it lit $3.85 of cash on fire for every $100 in revenue.

Final Judgment

We cheer for all companies solving complex technology issues, but in the case of Vishay Intertechnology, we’ll be cheering from the sidelines. With its shares topping the market in recent months, the stock trades at 30.3× forward P/E (or $16.66 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment. We’d recommend looking at a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than Vishay Intertechnology

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.