Shareholders of ICF International would probably like to forget the past six months even happened. The stock dropped 29.5% and now trades at $70.32. This may have investors wondering how to approach the situation.

Is now the time to buy ICF International, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Do We Think ICF International Will Underperform?

Even though the stock has become cheaper, we're cautious about ICF International. Here are three reasons why ICFI doesn't excite us and a stock we'd rather own.

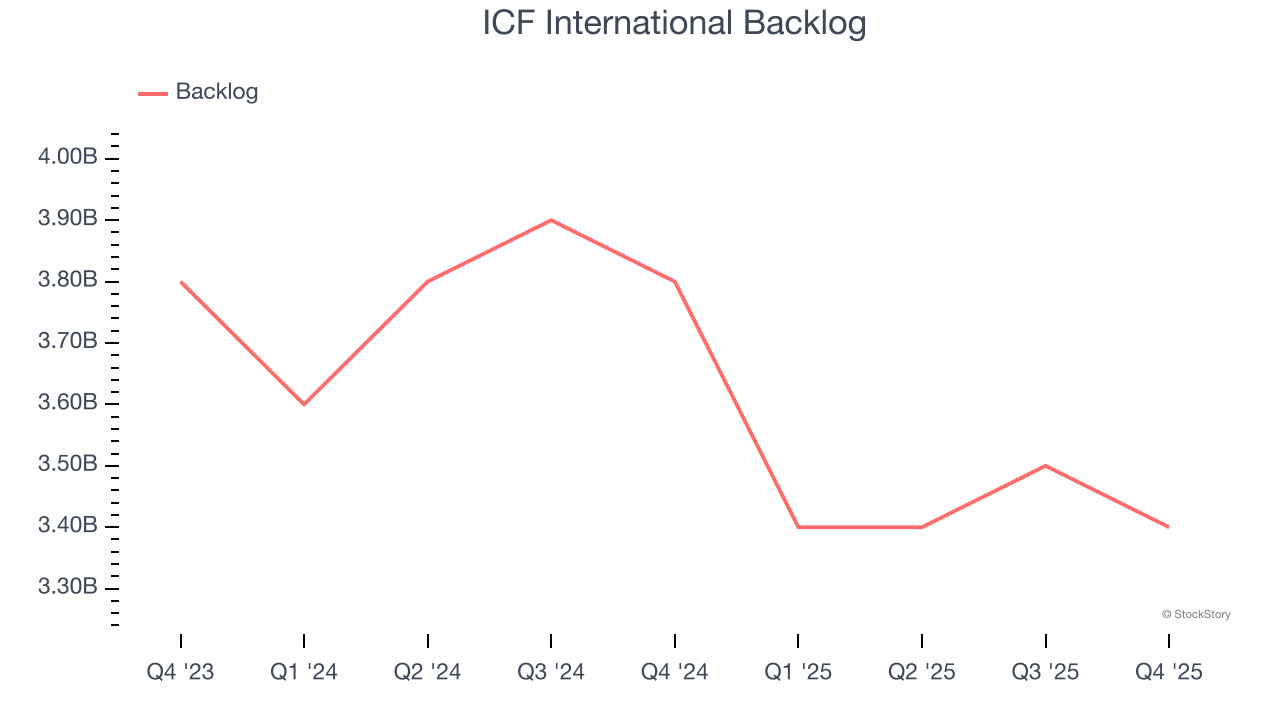

1. Backlog Declines as Orders Drop

We can better understand Government & Technical Consulting companies by analyzing their backlog. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into ICF International’s future revenue streams.

ICF International’s backlog came in at $3.4 billion in the latest quarter, and it averaged 7.4% year-on-year declines over the last two years. This performance was underwhelming and shows the company is not winning new orders. It also suggests there may be increasing competition or market saturation.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect ICF International’s revenue to rise by 2.2%. While this projection implies its newer products and services will spur better top-line performance, it is still below the sector average.

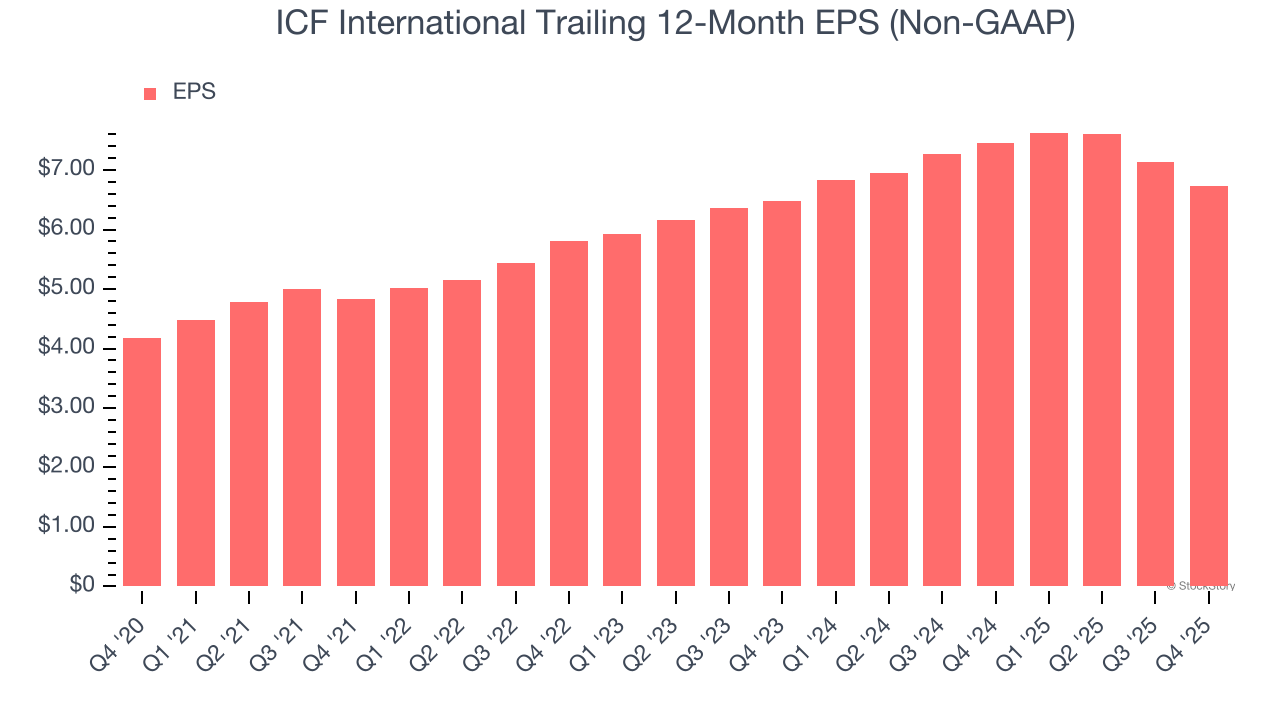

3. Recent EPS Growth Below Our Standards

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

ICF International’s EPS grew at a weak 2% compounded annual growth rate over the last two years. On the bright side, this performance was higher than its 2.3% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

Final Judgment

ICF International falls short of our quality standards. After the recent drawdown, the stock trades at 10.2× forward P/E (or $70.32 per share). This multiple tells us a lot of good news is priced in - we think there are better opportunities elsewhere. Let us point you toward a fast-growing restaurant franchise with an A+ ranch dressing sauce.

Stocks We Like More Than ICF International

ALSO WORTH WATCHING: Top 5 Momentum Stocks. The best time to own a great stock is when the market is finally noticing it. These aren't just high-quality businesses. Something is happening with them right now. Elite fundamentals meeting near-term momentum — both boxes checked at the same time.

Find out which stocks our AI platform is flagging this week. See this week's Strong Momentum stocks — FREE. Get Our Strong Momentum Stocks for Free HERE.

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.