Let’s dig into the relative performance of Monro (NASDAQ: MNRO) and its peers as we unravel the now-completed Q4 auto parts retailer earnings season.

Cars are complex machines that need maintenance and occasional repairs, and auto parts retailers cater to the professional mechanic as well as the do-it-yourself (DIY) fixer. Work on cars may entail replacing fluids, parts, or accessories, and these stores have the parts and accessories or these jobs. While e-commerce competition presents a risk, these stores have a leg up due to the combination of broad and deep selection as well as expertise provided by sales associates. Another change on the horizon could be the increasing penetration of electric vehicles.

The 5 auto parts retailer stocks we track reported a slower Q4. As a group, revenues were in line with analysts’ consensus estimates.

While some auto parts retailer stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 2.4% since the latest earnings results.

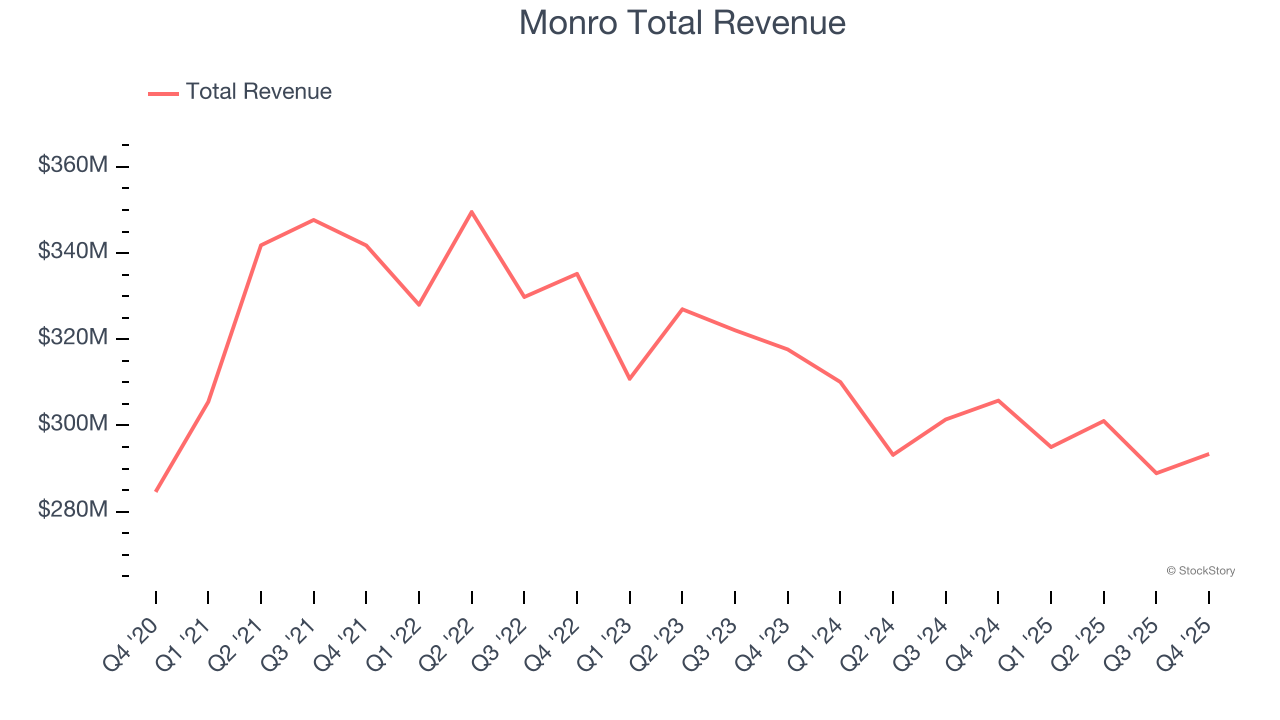

Monro (NASDAQ: MNRO)

Started as a single location in Rochester, New York, Monro (NASDAQ: MNRO) provides common auto services such as brake repairs, tire replacements, and oil changes.

Monro reported revenues of $293.4 million, down 4% year on year. This print fell short of analysts’ expectations by 0.6%, but it was still a strong quarter for the company with a beat of analysts’ EPS estimates and a decent beat of analysts’ EBITDA estimates.

“After we saw some softness in consumer demand in October, the Monro team drove growth in comparable store sales in November and December. Further, when adjusting for a shift in the timing of the Christmas holiday in the prior year, the months of November and December as well as the third quarter, mark the first time we delivered positive comps on a 2-year stack in over two years. This has also enabled us to report our fourth consecutive quarter of positive comps for the first time in several years. We believe we were able to take share in our tire category as soon as winter hit as our stores were well-prepared with proper staffing, an updated tire assortment, and additional marketing spend. For the second quarter in a row, we delivered solid gross margin performance with a gross margin rate that expanded 60 basis points year-over-year to 34.9%. We also re-invested the selling, general, and administrative expense savings from our closed stores into additional marketing to support topline growth. For the third quarter in a row, we reduced inventory levels across the system, this time by over $7 million. We have now achieved an overall inventory reduction of more than $28 million, which is 16% since the end of March, just nine months ago. This is a clear indication of how we’ve continued to manage our inventories more efficiently in fiscal 2026”, said Peter Fitzsimmons, President and Chief Executive Officer.

Monro delivered the slowest revenue growth of the whole group. Interestingly, the stock is up 12.8% since reporting and currently trades at $22.59.

Is now the time to buy Monro? Access our full analysis of the earnings results here, it’s free.

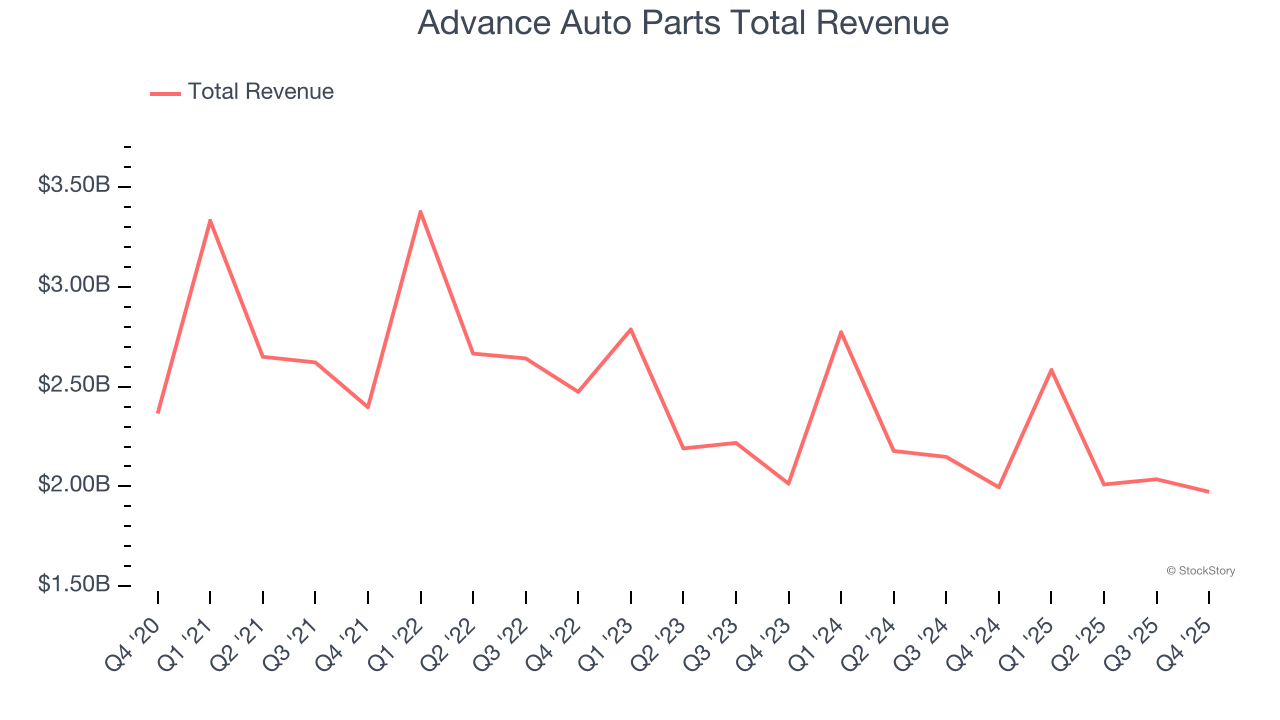

Best Q4: Advance Auto Parts (NYSE: AAP)

Founded in Virginia in 1932, Advance Auto Parts (NYSE: AAP) is an auto parts and accessories retailer that sells everything from carburetors to motor oil to car floor mats.

Advance Auto Parts reported revenues of $1.97 billion, down 1.2% year on year, outperforming analysts’ expectations by 1%. The business had a strong quarter with a beat of analysts’ EPS estimates and full-year EPS guidance exceeding analysts’ expectations.

Advance Auto Parts achieved the biggest analyst estimates beat and highest full-year guidance raise among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 3.8% since reporting. It currently trades at $55.99.

Is now the time to buy Advance Auto Parts? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: AutoZone (NYSE: AZO)

Aiming to be a one-stop shop for the DIY customer, AutoZone (NYSE: AZO) is an auto parts and accessories retailer that sells everything from car batteries to windshield wiper fluid to brake pads.

AutoZone reported revenues of $4.63 billion, up 8.2% year on year, in line with analysts’ expectations. It was a slower quarter as it posted a miss of analysts’ EBITDA estimates and a significant miss of analysts’ EPS estimates.

The stock is flat since the results and currently trades at $3,745.

Read our full analysis of AutoZone’s results here.

Genuine Parts (NYSE: GPC)

Largely targeting the professional customer, Genuine Parts (NYSE: GPC) sells auto and industrial parts such as batteries, belts, bearings, and machine fluids.

Genuine Parts reported revenues of $6.01 billion, up 4.1% year on year. This print missed analysts’ expectations by 0.8%. Overall, it was a softer quarter as it also logged full-year EPS guidance missing analysts’ expectations significantly and a significant miss of analysts’ EBITDA estimates.

Genuine Parts had the weakest performance against analyst estimates among its peers. The stock is down 18.6% since reporting and currently trades at $119.78.

Read our full, actionable report on Genuine Parts here, it’s free.

O'Reilly (NASDAQ: ORLY)

Serving both the DIY customer and professional mechanic, O’Reilly Automotive (NASDAQ: ORLY) is an auto parts and accessories retailer that sells everything from fuel pumps to car air fresheners to mufflers.

O'Reilly reported revenues of $4.41 billion, up 7.8% year on year. This number met analysts’ expectations. However, it was a slower quarter as it produced full-year EPS guidance missing analysts’ expectations and full-year revenue guidance slightly missing analysts’ expectations.

O'Reilly had the weakest full-year guidance update among its peers. The stock is down 1.8% since reporting and currently trades at $95.

Read our full, actionable report on O'Reilly here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Top 5 Quality Compounder Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.