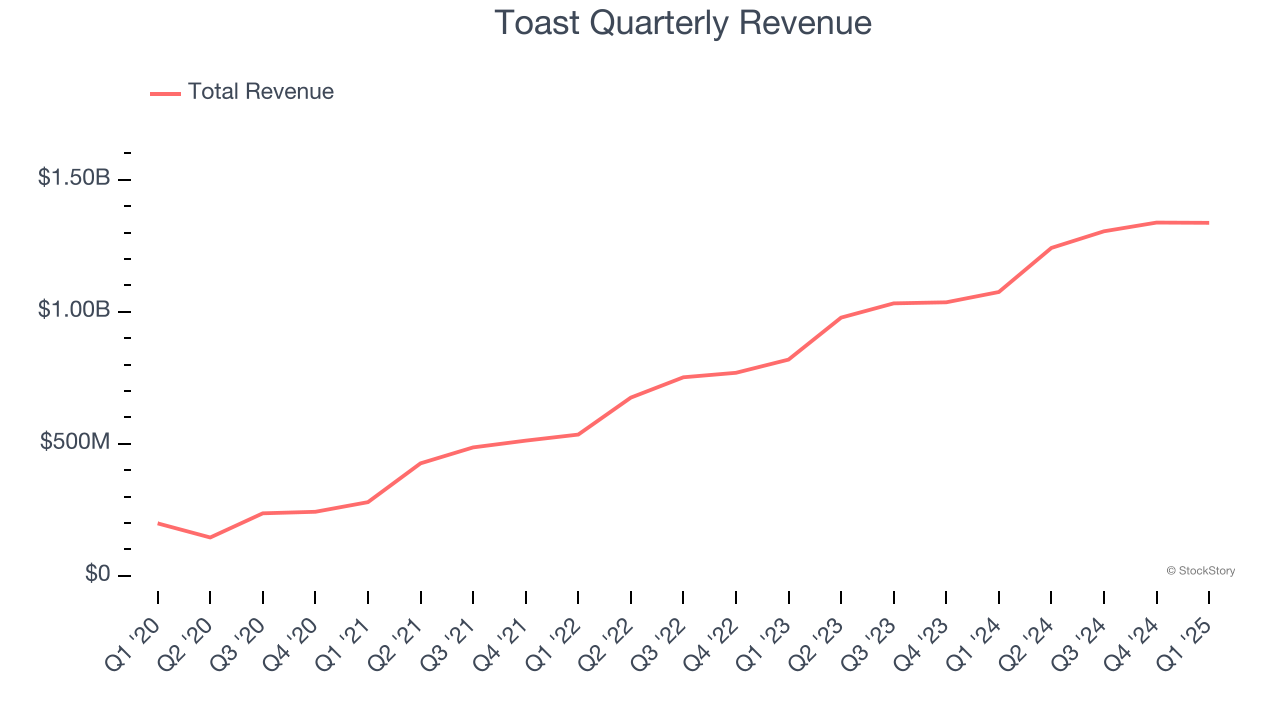

Restaurant software platform Toast (NYSE: TOST) missed Wall Street’s revenue expectations in Q1 CY2025, but sales rose 24.4% year on year to $1.34 billion. Its non-GAAP profit of $0.09 per share was 51.6% below analysts’ consensus estimates.

Is now the time to buy Toast? Find out by accessing our full research report, it’s free.

Toast (TOST) Q1 CY2025 Highlights:

- Revenue: $1.34 billion vs analyst estimates of $1.35 billion (24.4% year-on-year growth, 0.8% miss)

- Adjusted EBITDA: $133 million vs analyst estimates of $106.2 million (9.9% margin, 25.2% beat)

- EBITDA guidance for the full year is $550 million at the midpoint, above analyst estimates of $524.9 million

- Operating Margin: 3.2%, up from -5.2% in the same quarter last year

- Free Cash Flow Margin: 5.2%, down from 10% in the previous quarter

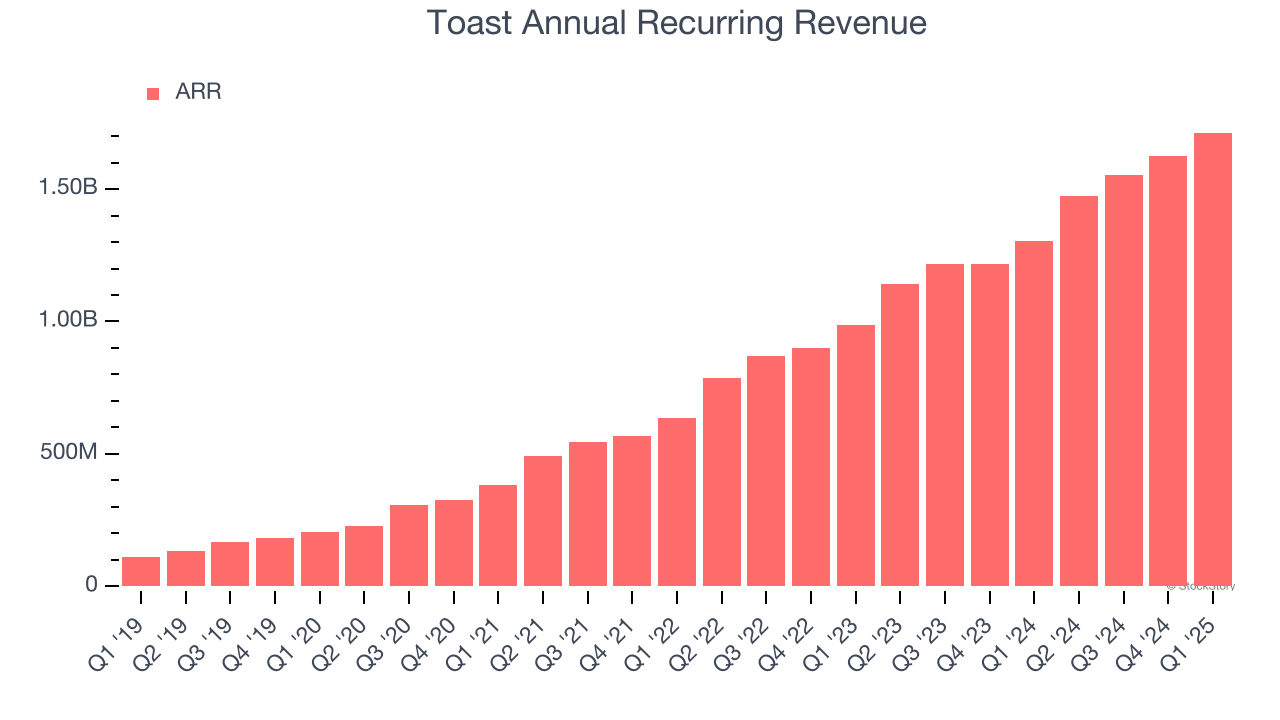

- Annual Recurring Revenue: $1.71 billion at quarter end, up 31.3% year on year

- Market Capitalization: $20.55 billion

Company Overview

Founded by three MIT engineers at a local Cambridge bar, Toast (NYSE: TOST) provides integrated point-of-sale (POS) hardware, software, and payments solutions for restaurants.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Toast’s 38.6% annualized revenue growth over the last three years was exceptional. Its growth beat the average software company and shows its offerings resonate with customers, a helpful starting point for our analysis.

This quarter, Toast generated an excellent 24.4% year-on-year revenue growth rate, but its $1.34 billion of revenue fell short of Wall Street’s high expectations.

Looking ahead, sell-side analysts expect revenue to grow 21.9% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is commendable and implies the market is forecasting success for its products and services.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Annual Recurring Revenue

While reported revenue for a software company can include low-margin items like implementation fees, annual recurring revenue (ARR) is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Toast’s ARR punched in at $1.71 billion in Q1, and over the last four quarters, its growth was fantastic as it averaged 30.4% year-on-year increases. This alternate topline metric grew faster than total sales, which likely means that the recurring portions of the business are growing faster than less predictable, choppier ones such as implementation fees. That could be a good sign for future revenue growth.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Toast’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a competitive market and must continue investing to grow.

Key Takeaways from Toast’s Q1 Results

We were impressed by Toast’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. On the other hand, its revenue slightly missed. Zooming out, we still think this was a solid print. The stock traded up 3.9% to $38.02 immediately after reporting.

Toast may have had a good quarter, but does that mean you should invest right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.