As the Q4 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the aerospace industry, including Curtiss-Wright (NYSE: CW) and its peers.

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

The 14 aerospace stocks we track reported a mixed Q4. As a group, revenues along with next quarter’s revenue guidance were in line with analysts’ consensus estimates.

Amidst this news, share prices of the companies have had a rough stretch. On average, they are down 19% since the latest earnings results.

Curtiss-Wright (NYSE: CW)

Formed from a merger of 12 companies, Curtiss-Wright (NYSE: CW) provides a range of products and services to the aerospace, industrial, electronic, and maritime industries.

Curtiss-Wright reported revenues of $824.3 million, up 4.9% year on year. This print exceeded analysts’ expectations by 5.9%. Overall, it was a very strong quarter for the company with full-year EPS guidance exceeding analysts’ expectations.

"Curtiss-Wright concluded the year with a strong, fourth quarter financial performance that reflected better-than-expected sales growth, record quarterly Adjusted diluted EPS of $3.27, strong free cash flow and robust order activity," said Lynn M. Bamford, Chair and CEO of Curtiss-Wright Corporation.

The stock is down 20.5% since reporting and currently trades at $271.33.

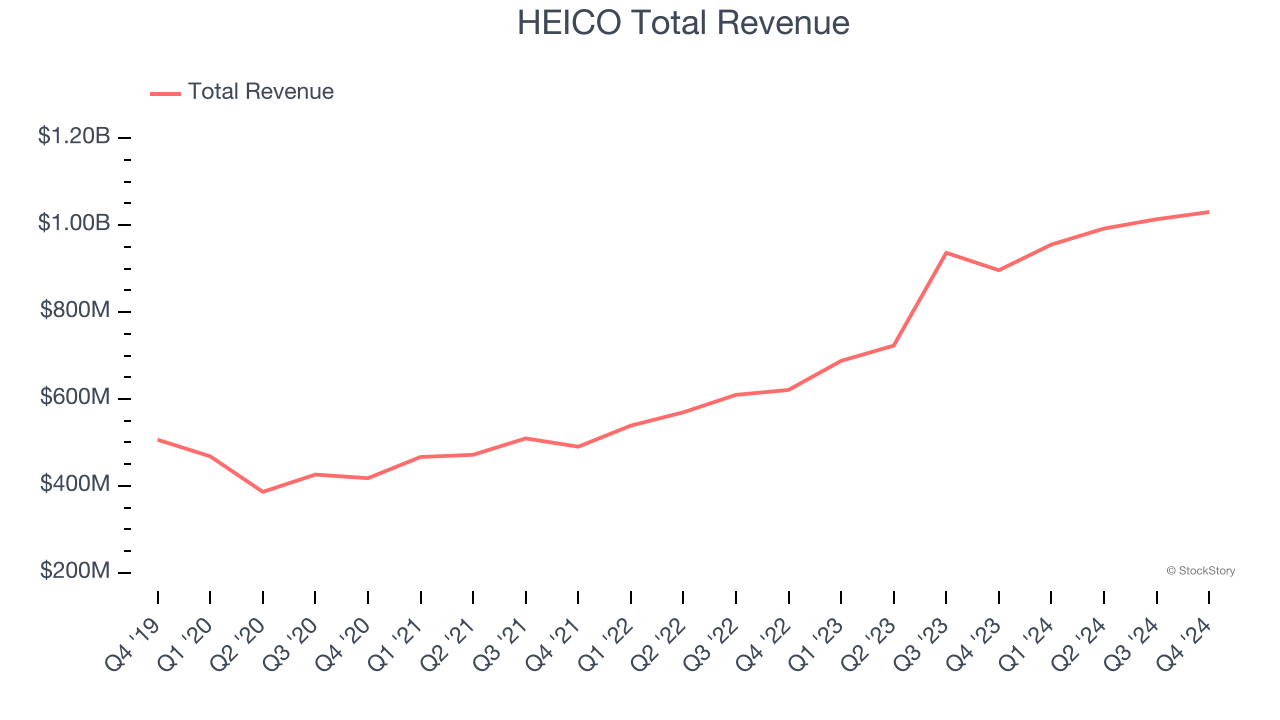

Best Q4: HEICO (NYSE: HEI)

Founded in 1957, HEICO (NYSE: HEI) manufactures and services aerospace and electronic components for commercial aviation, defense, space, and other industries.

HEICO reported revenues of $1.03 billion, up 14.9% year on year, outperforming analysts’ expectations by 5.4%. The business had an incredible quarter with a solid beat of analysts’ organic revenue estimates and an impressive beat of analysts’ EPS estimates.

The market seems content with the results as the stock is up 4% since reporting. It currently trades at $237.

Is now the time to buy HEICO? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Boeing (NYSE: BA)

One of the companies that forms a duopoly in the commercial aircraft market, Boeing (NYSE: BA) develops, manufactures, and services commercial airplanes, defense products, and space systems.

Boeing reported revenues of $15.24 billion, down 30.8% year on year, falling short of analysts’ expectations by 6.4%. It was a disappointing quarter as it posted a significant miss of analysts’ adjusted operating income estimates.

Boeing delivered the slowest revenue growth in the group. As expected, the stock is down 25.1% since the results and currently trades at $131.19.

Read our full analysis of Boeing’s results here.

Redwire (NYSE: RDW)

Based in Jacksonville, Florida, Redwire (NYSE: RDW) is a provider of systems and components used in space infrastructure.

Redwire reported revenues of $69.56 million, up 9.6% year on year. This result missed analysts’ expectations by 6.7%. Taking a step back, it was a mixed quarter as it also logged full-year EBITDA guidance exceeding analysts’ expectations.

Redwire achieved the highest full-year guidance raise but had the weakest performance against analyst estimates among its peers. The stock is down 39.4% since reporting and currently trades at $6.82.

Read our full, actionable report on Redwire here, it’s free.

Howmet (NYSE: HWM)

Inventing the first forged aluminum truck wheel, Howmet (NYSE: HWM) specializes in lightweight metals engineering and manufacturing multi-material components used in vehicles.

Howmet reported revenues of $1.89 billion, up 9.2% year on year. This number beat analysts’ expectations by 0.7%. Aside from that, it was a mixed quarter as it also recorded EBITDA guidance for next quarter beating analysts’ expectations.

The stock is down 18.2% since reporting and currently trades at $104.77.

Read our full, actionable report on Howmet here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.