The past six months haven’t been great for Merck. It just made a new 52-week low of $79.69, and shareholders have lost 26.6% of their capital. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Given the weaker price action, is now the time to buy MRK? Find out in our full research report, it’s free.

Why Does Merck Spark Debate?

With roots dating back to 1891 and a portfolio that includes the blockbuster cancer immunotherapy Keytruda, Merck (NYSE: MRK) develops and sells prescription medicines, vaccines, and animal health products across oncology, infectious diseases, cardiovascular, and other therapeutic areas.

Two Things to Like:

1. Economies of Scale Give It Negotiating Leverage with Suppliers

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

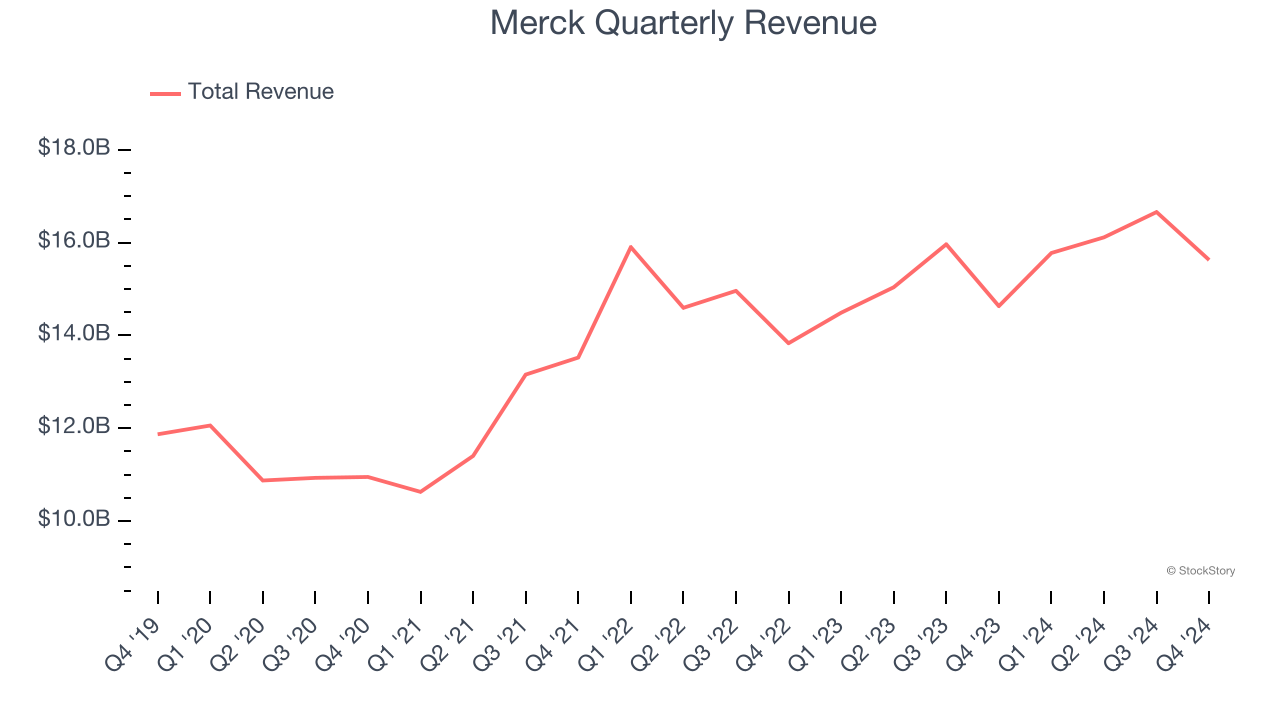

With $64.17 billion in revenue over the past 12 months, Merck is one of the most scaled enterprises in healthcare. This is particularly important because branded pharmaceuticals companies are volume-driven businesses due to their low margins.

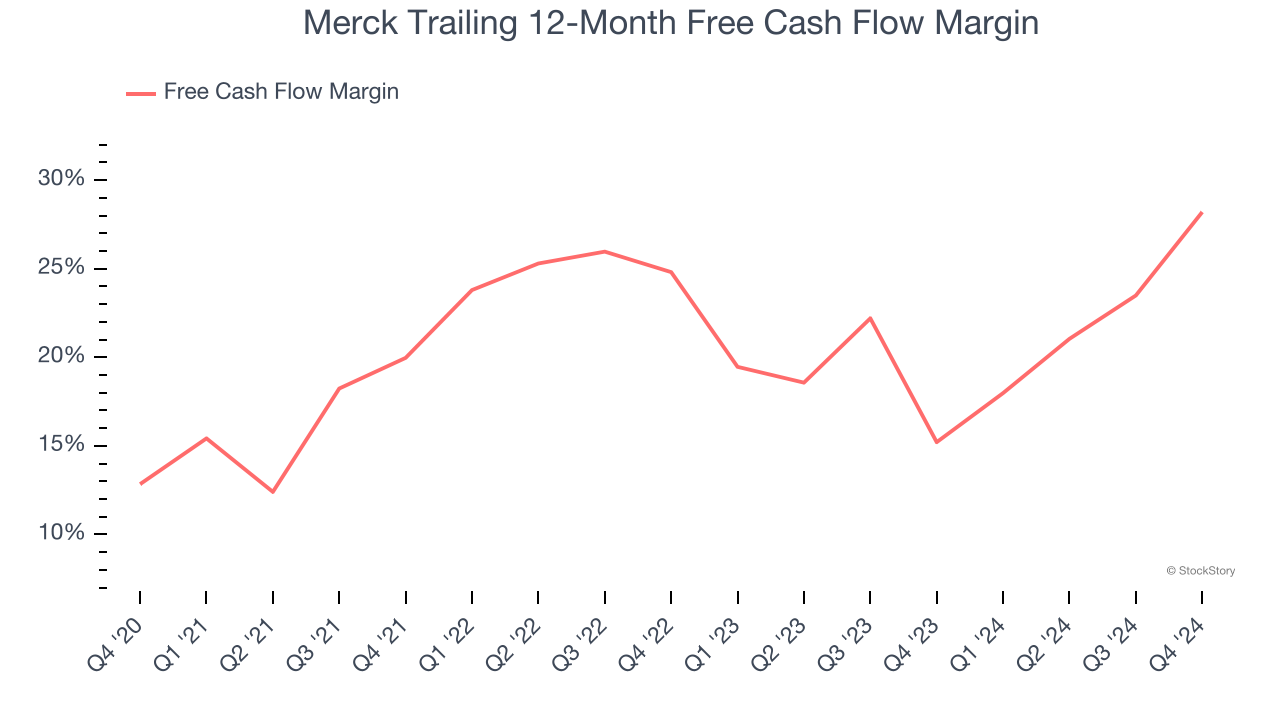

2. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Merck’s margin expanded by 15.4 percentage points over the last five years. This is encouraging because it gives the company more optionality. Merck’s free cash flow margin for the trailing 12 months was 28.2%.

One Reason to be Careful:

Long-Term Revenue Growth Disappoints

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Merck’s sales grew at a mediocre 6.5% compounded annual growth rate over the last five years. This wasn’t a great result compared to the rest of the healthcare sector, but there are still things to like about Merck.

Final Judgment

Merck’s positive characteristics outweigh the negatives. After the recent drawdown, the stock trades at 9.1× forward price-to-earnings (or $79.69 per share). Is now a good time to buy? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Merck

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.