Over the past six months, ServisFirst Bancshares’s shares (currently trading at $73.63) have posted a disappointing 5% loss, well below the S&P 500’s 11.7% gain. This was partly driven by its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy ServisFirst Bancshares, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free for active Edge members.

Why Is ServisFirst Bancshares Not Exciting?

Even though the stock has become cheaper, we're swiping left on ServisFirst Bancshares for now. Here are three reasons we avoid SFBS and a stock we'd rather own.

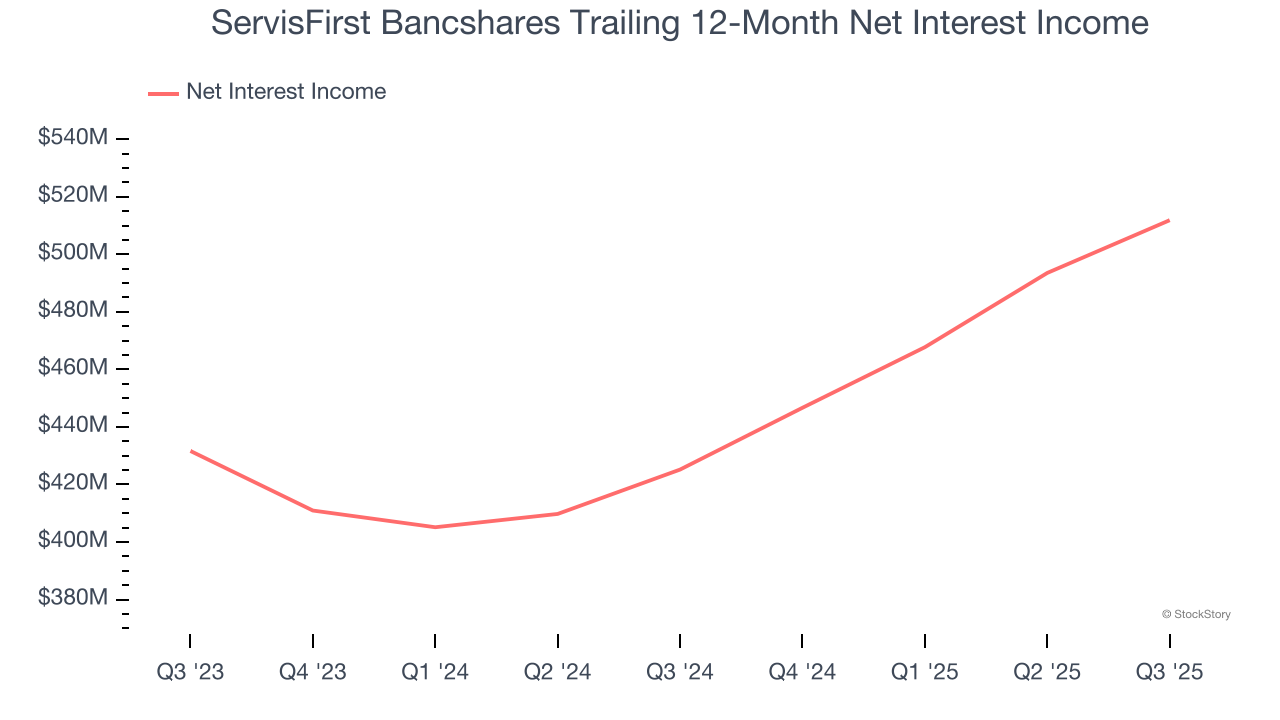

1. Net Interest Income Points to Soft Demand

While bank generate revenue from multiple sources, investors view net interest income as a cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of one-time fees.

ServisFirst Bancshares’s net interest income has grown at a 9.7% annualized rate over the last five years, slightly worse than the broader banking industry and in line with its total revenue.

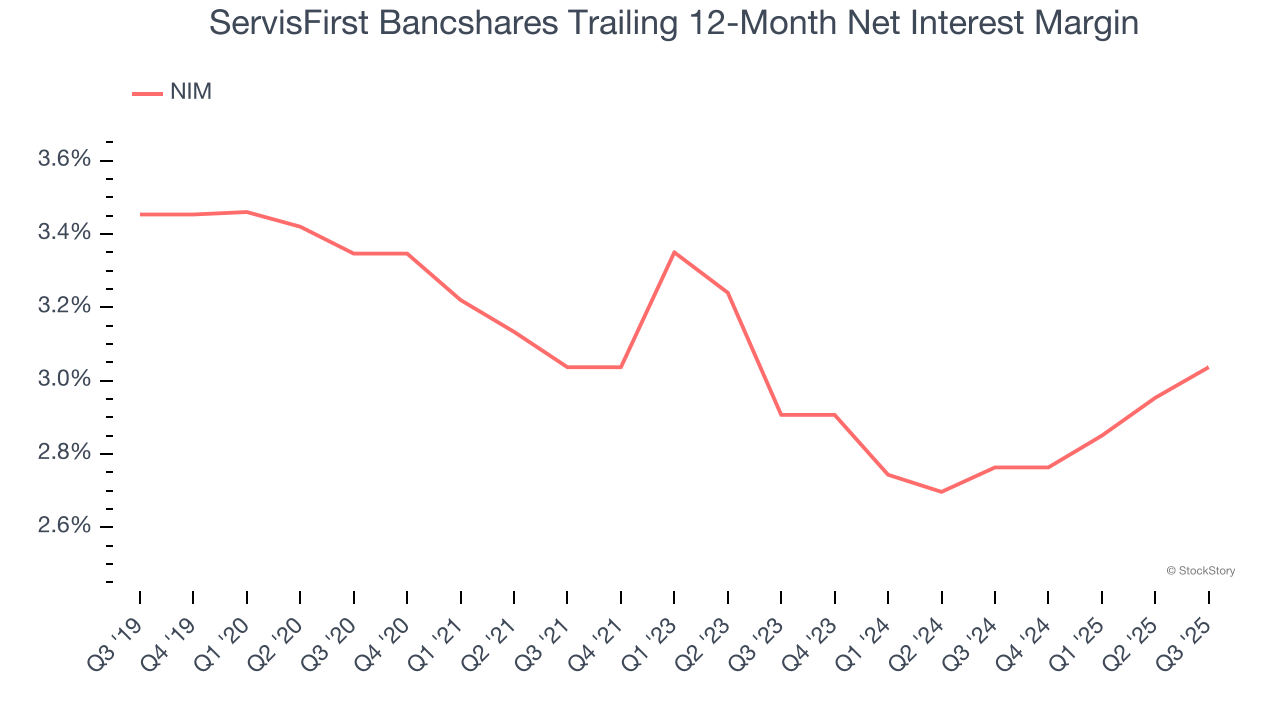

2. Low Net Interest Margin Reveals Weak Loan Book Profitability

Net interest margin (NIM) represents the unit economics of a bank by measuring the profitability of its interest-bearing assets relative to its interest-bearing liabilities. It's a fundamental metric that investors use to assess lending premiums and returns.

Over the past two years, we can see that ServisFirst Bancshares’s net interest margin averaged a weak 2.9%, indicating the company has weak loan book economics.

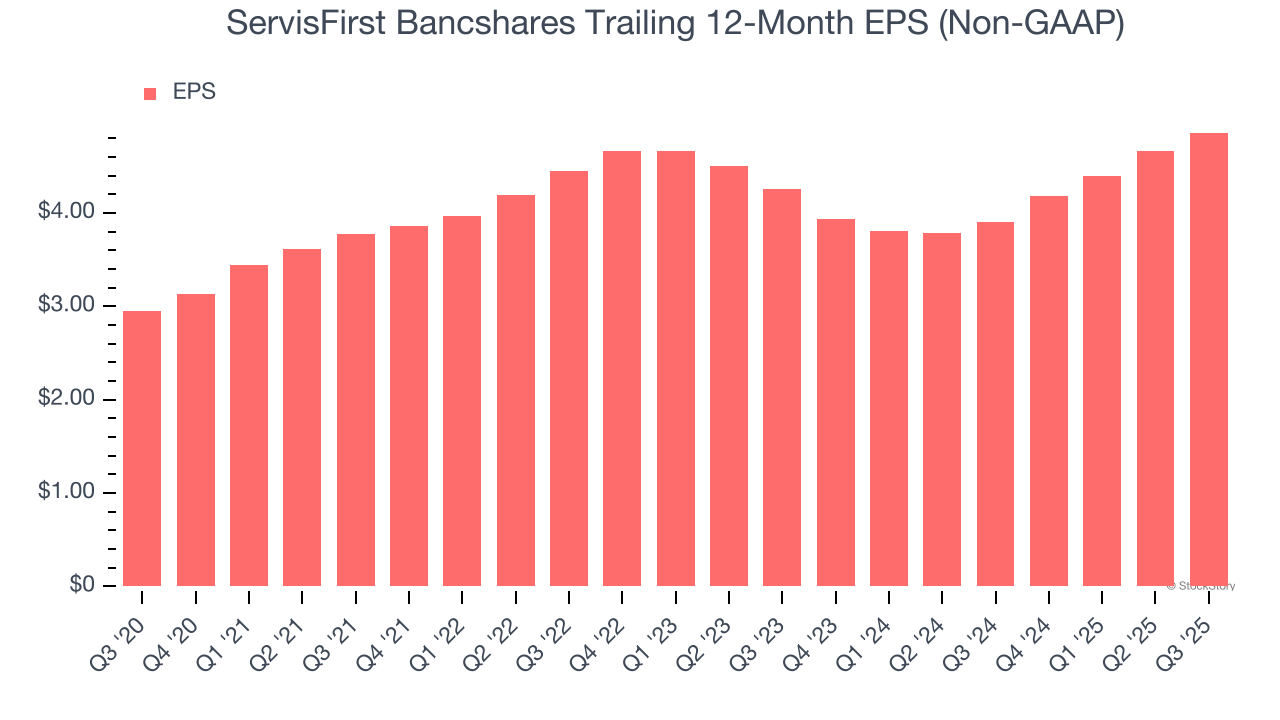

3. Recent EPS Growth Below Our Standards

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

ServisFirst Bancshares’s EPS grew at an unimpressive 6.8% compounded annual growth rate over the last two years, lower than its 9% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

ServisFirst Bancshares isn’t a terrible business, but it doesn’t pass our quality test. Following the recent decline, the stock trades at 2.2× forward P/B (or $73.63 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at the most entrenched endpoint security platform on the market.

Stocks We Would Buy Instead of ServisFirst Bancshares

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.