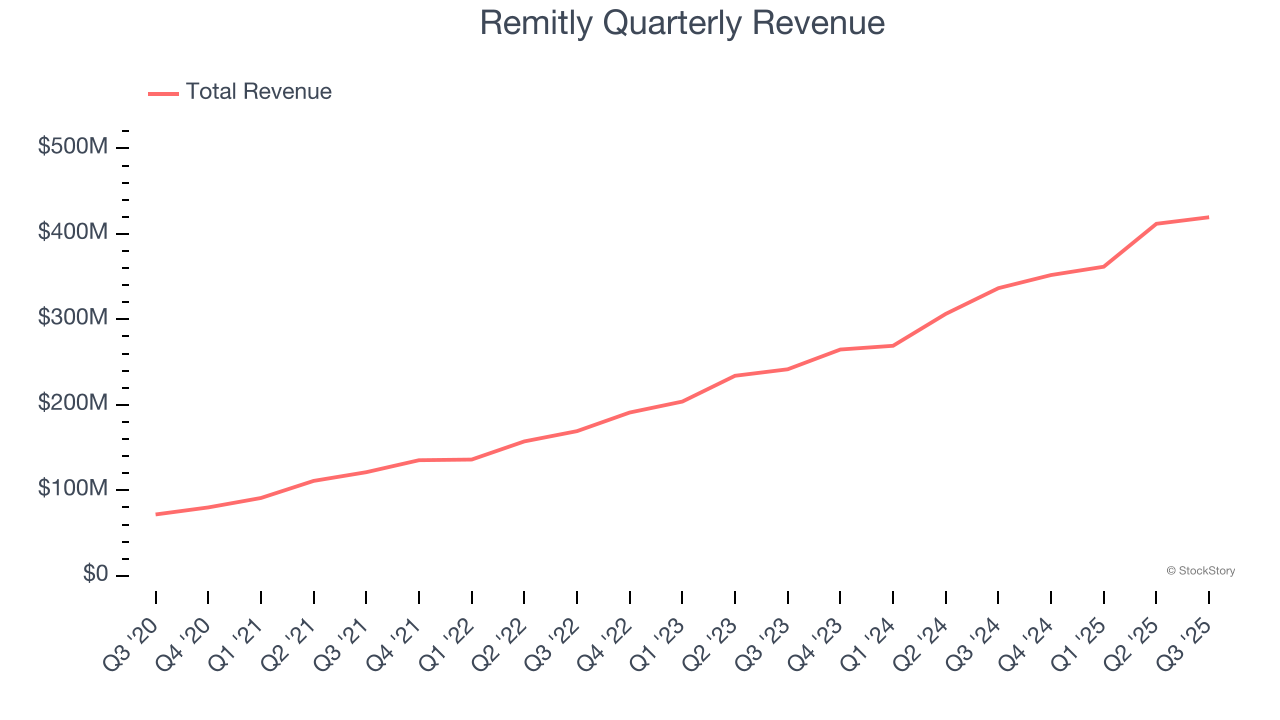

Online money transfer platform Remitly (NASDAQ: RELY) announced better-than-expected revenue in Q3 CY2025, with sales up 24.7% year on year to $419.5 million. On the other hand, next quarter’s revenue guidance of $427 million was less impressive, coming in 0.8% below analysts’ estimates. Its GAAP profit of $0.04 per share was $0.01 above analysts’ consensus estimates.

Is now the time to buy Remitly? Find out by accessing our full research report, it’s free for active Edge members.

Remitly (RELY) Q3 CY2025 Highlights:

- Revenue: $419.5 million vs analyst estimates of $413.7 million (24.7% year-on-year growth, 1.4% beat)

- EPS (GAAP): $0.04 vs analyst estimates of $0.03 ($0.01 beat)

- Adjusted EBITDA: $61.18 million vs analyst estimates of $54.9 million (14.6% margin, 11.4% beat)

- Revenue Guidance for Q4 CY2025 is $427 million at the midpoint, below analyst estimates of $430.6 million

- EBITDA guidance for the full year is $235 million at the midpoint, above analyst estimates of $230.1 million

- Operating Margin: 2.8%, up from 0.1% in the same quarter last year

- Free Cash Flow Margin: 0.4%, down from 6.9% in the previous quarter

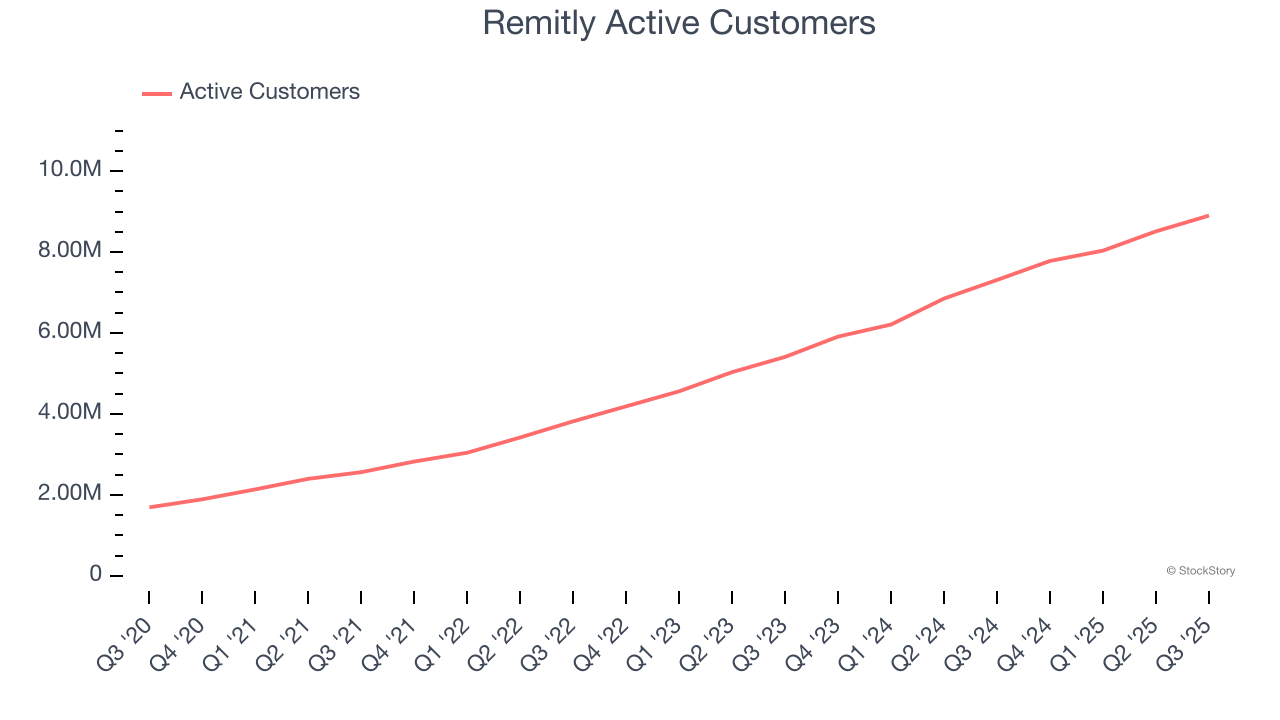

- Active Customers: 8.9 million, up 1.59 million year on year

- Market Capitalization: $3.34 billion

“In Q3, we built on the momentum from last quarter, delivering innovation across the product portfolio,” said Matt Oppenheimer, co-founder and Chief Executive Officer, Remitly.

Company Overview

With Amazon founder Jeff Bezos as an early investor, Remitly (NASDAQ: RELY) is an online platform that enables consumers to safely and quickly send money globally.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Remitly grew its sales at an incredible 37.2% compounded annual growth rate. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Remitly reported robust year-on-year revenue growth of 24.7%, and its $419.5 million of revenue topped Wall Street estimates by 1.4%. Company management is currently guiding for a 21.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 19.8% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is admirable and implies the market is baking in success for its products and services.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Active Customers

Customer Growth

As a fintech company, Remitly generates revenue growth by increasing both the number of users on its platform and the number of transactions they execute.

Over the last two years, Remitly’s active customers, a key performance metric for the company, increased by 32% annually to 8.9 million in the latest quarter. This growth rate is among the fastest of any consumer internet business and indicates its offerings have significant traction.

In Q3, Remitly added 1.59 million active customers, leading to 21.8% year-on-year growth. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t accelerating customer growth just yet.

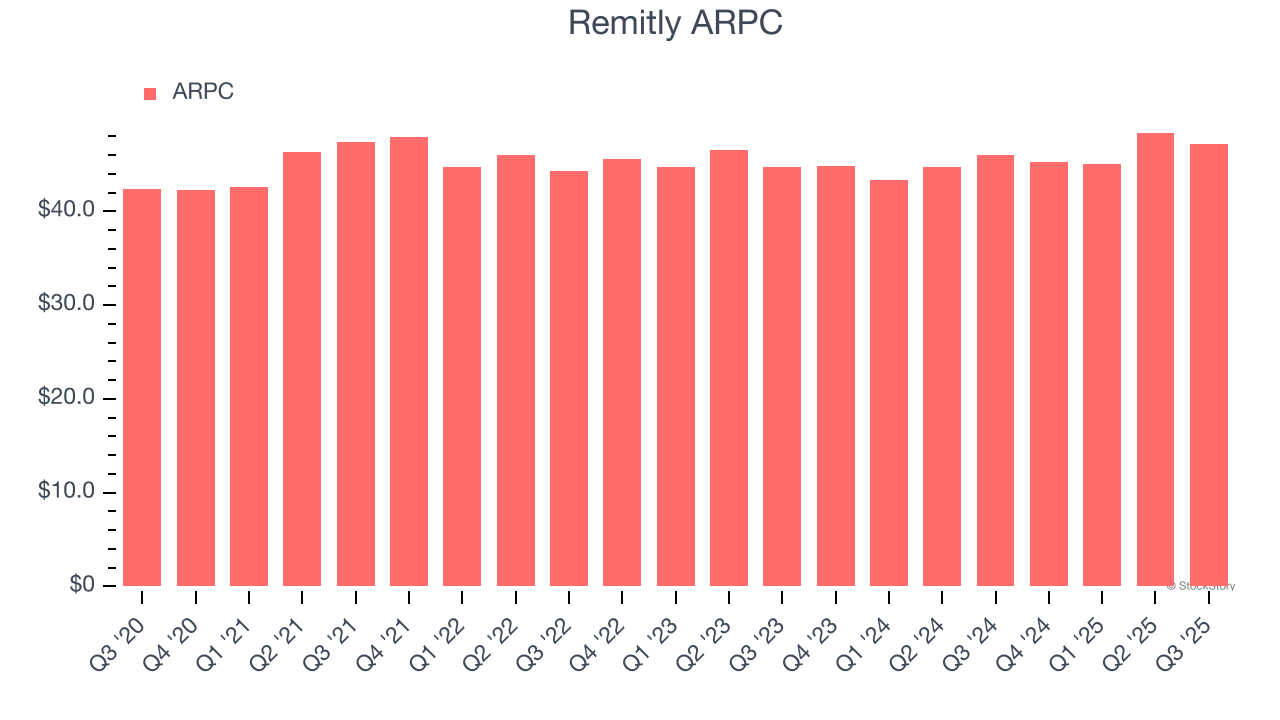

Revenue Per Customer

Average revenue per customer (ARPC) is a critical metric to track because it measures how much the company earns in fees from each user. ARPC also gives us unique insights into the average transaction size on Remitly’s platform and the company’s take rate, or "cut", on each transaction.

Remitly’s ARPC growth has been subpar over the last two years, averaging 1.2%. This isn’t great, but the increase in active customers is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Remitly tries boosting ARPC by taking a more aggressive approach to monetization, it’s unclear whether customers can continue growing at the current pace.

This quarter, Remitly’s ARPC clocked in at $47.13. It grew by 2.4% year on year, slower than its customer growth.

Key Takeaways from Remitly’s Q3 Results

We were impressed by how significantly Remitly blew past analysts’ EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next quarter slightly missed and its EBITDA guidance for next quarter also fell short of Wall Street’s estimates, and this weighed on shares. The stock traded down 13.3% to $14.28 immediately following the results.

So should you invest in Remitly right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.