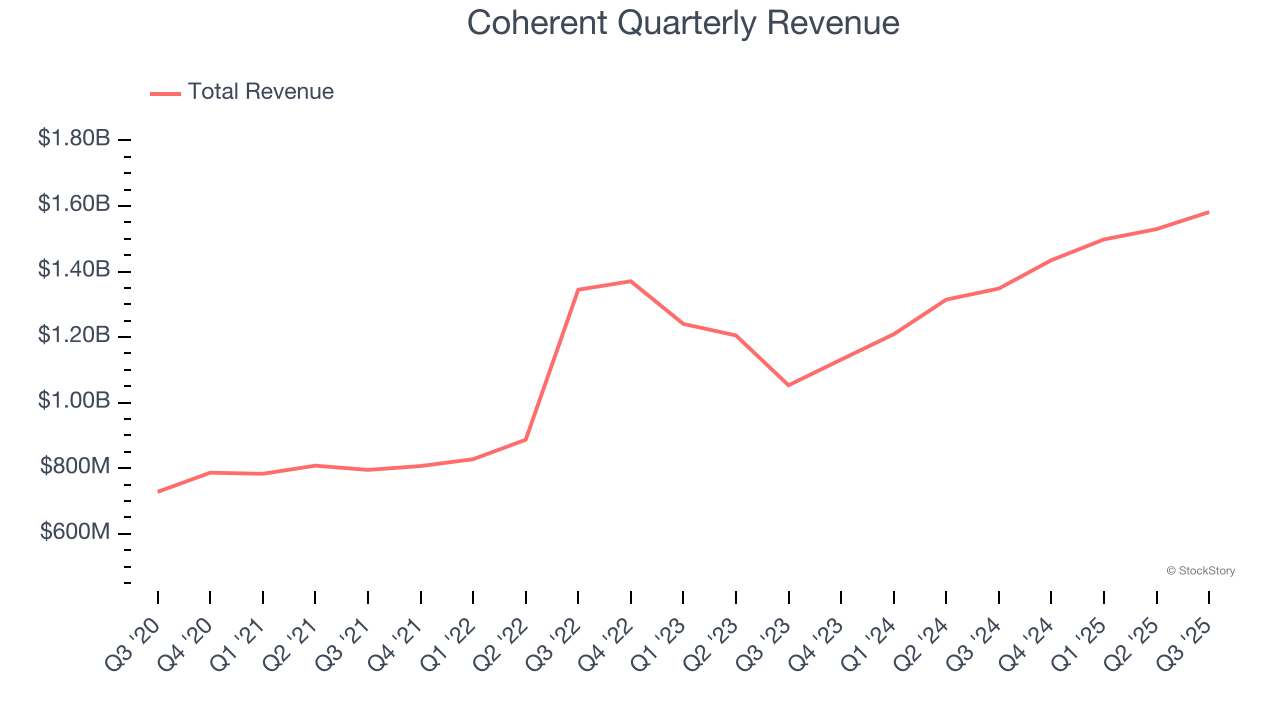

Materials and photonics company Coherent (NYSE: COHR) announced better-than-expected revenue in Q3 CY2025, with sales up 17.3% year on year to $1.58 billion. On top of that, next quarter’s revenue guidance ($1.63 billion at the midpoint) was surprisingly good and 4.9% above what analysts were expecting. Its non-GAAP profit of $1.16 per share was 11.3% above analysts’ consensus estimates.

Is now the time to buy Coherent? Find out by accessing our full research report, it’s free for active Edge members.

Coherent (COHR) Q3 CY2025 Highlights:

- Revenue: $1.58 billion vs analyst estimates of $1.53 billion (17.3% year-on-year growth, 3.1% beat)

- Adjusted EPS: $1.16 vs analyst estimates of $1.04 (11.3% beat)

- Adjusted Operating Income: $308.9 million vs analyst estimates of $286 million (19.5% margin, 8% beat)

- Revenue Guidance for Q4 CY2025 is $1.63 billion at the midpoint, above analyst estimates of $1.55 billion

- Adjusted EPS guidance for Q4 CY2025 is $1.20 at the midpoint, above analyst estimates of $1.12

- Operating Margin: 13.7%, up from 5.6% in the same quarter last year

- Free Cash Flow was -$57.9 million, down from $61 million in the same quarter last year

- Market Capitalization: $20.2 billion

Jim Anderson, CEO, said, “Revenue growth of 19% year-over-year in the September quarter on a pro forma basis was driven by strong demand from AI-related datacenters and communications. We expect continued strong growth throughout this fiscal year based on increasing datacenter and communications demand along with our continued production capacity expansion.”

Company Overview

Created through the 2022 rebranding of II-VI Incorporated, a company with roots dating back to 1971, Coherent (NYSE: COHR) develops and manufactures advanced materials, lasers, and optical components for applications ranging from telecommunications to industrial manufacturing.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can have short-term success, but a top-tier one grows for years.

With $6.04 billion in revenue over the past 12 months, Coherent is one of the larger companies in the business services industry and benefits from a well-known brand that influences purchasing decisions.

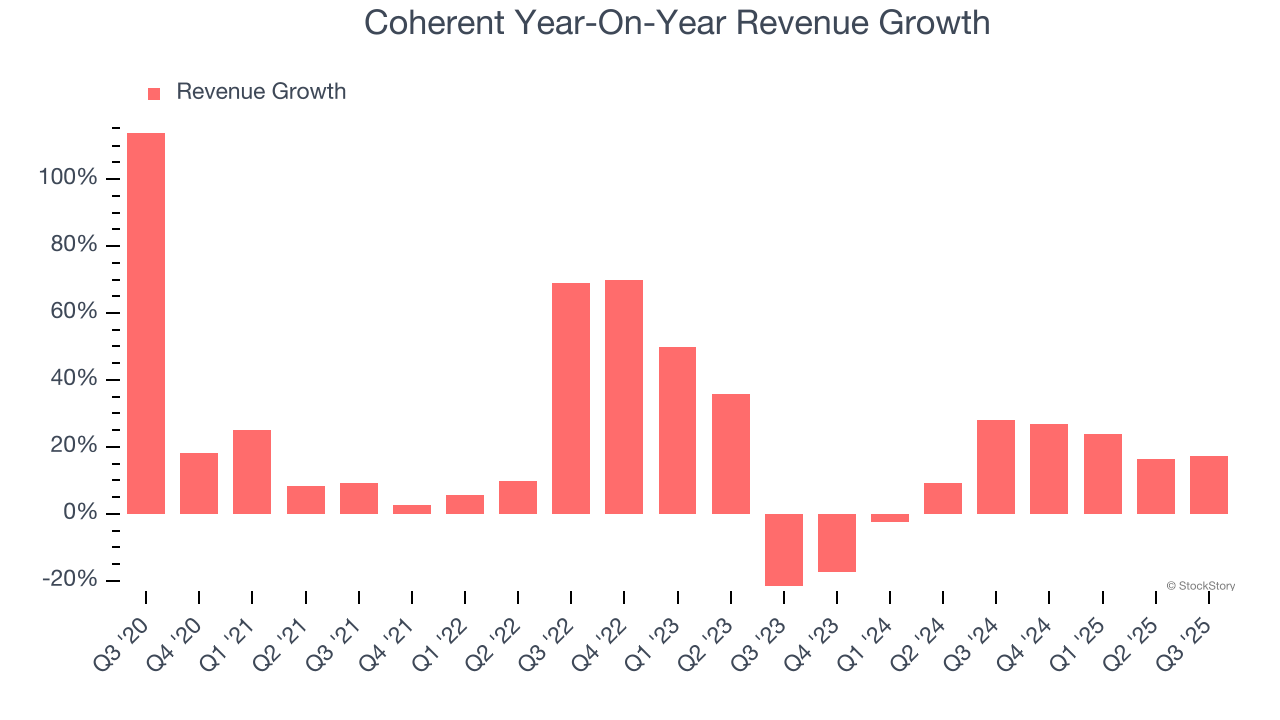

As you can see below, Coherent’s 16.9% annualized revenue growth over the last five years was incredible. This is an encouraging starting point for our analysis because it shows Coherent’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Coherent’s annualized revenue growth of 11.4% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

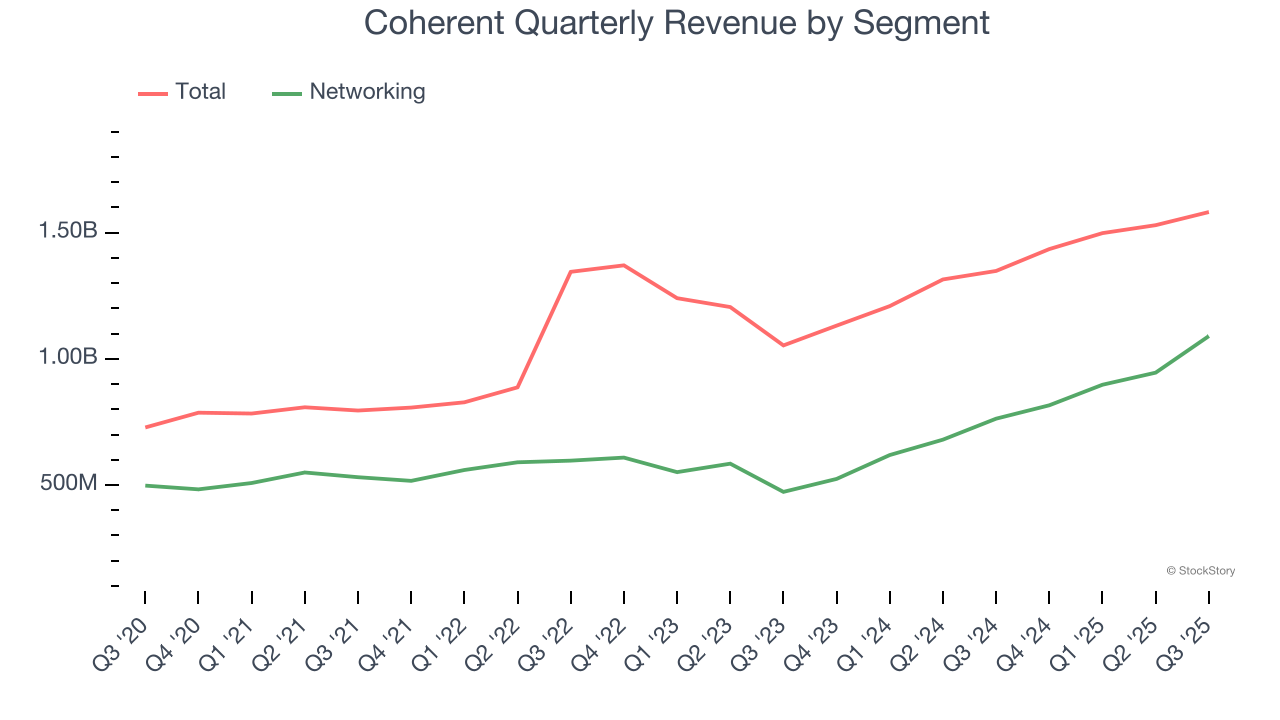

Coherent also breaks out the revenue for its most important segment, Networking. Over the last two years, Coherent’s Networking revenue (communications components and subsystems) averaged 32.3% year-on-year growth. This segment has outperformed its total sales during the same period, lifting the company’s performance.

This quarter, Coherent reported year-on-year revenue growth of 17.3%, and its $1.58 billion of revenue exceeded Wall Street’s estimates by 3.1%. Company management is currently guiding for a 13.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 7.3% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is healthy and suggests the market sees success for its products and services.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Adjusted Operating Margin

Adjusted operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D. It also removes various one-time costs to paint a better picture of normalized profits.

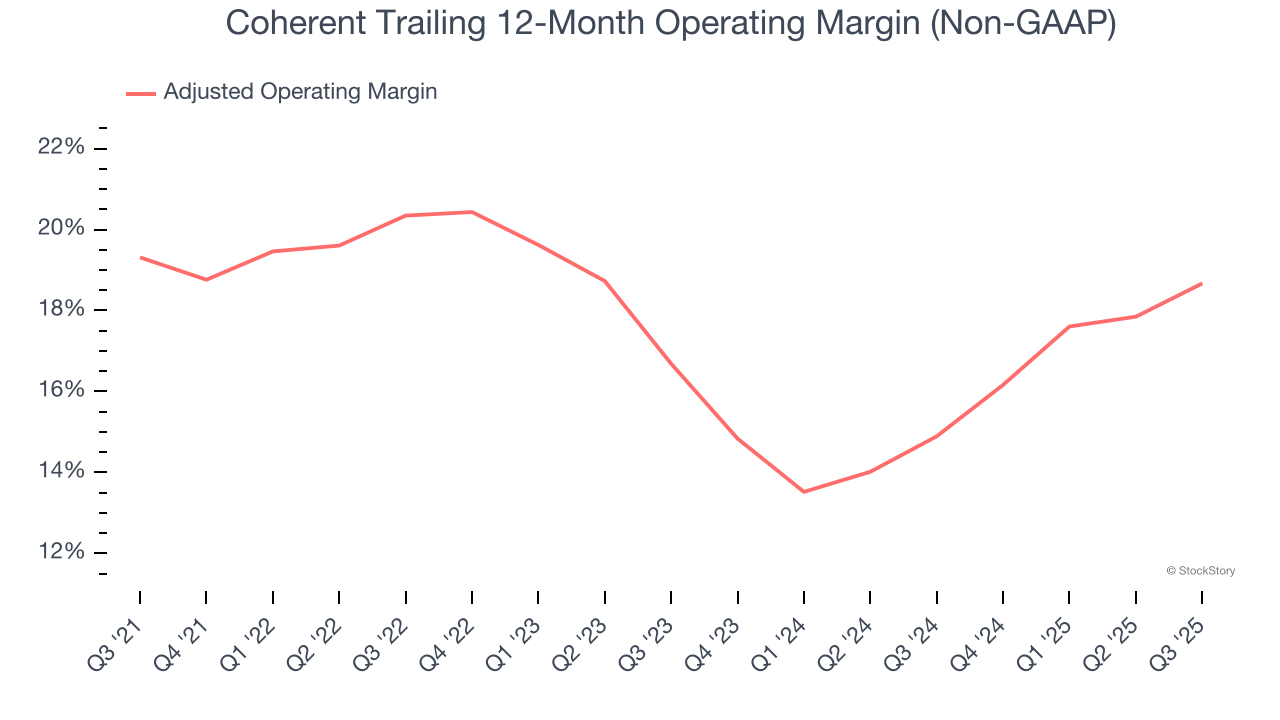

Coherent’s adjusted operating margin has been trending up over the last 12 months and averaged 17.8% over the last five years. On top of that, its profitability was top-notch for a business services business, showing it’s an well-run company that manages its expenses efficiently and benefits from immense operating leverage as it scales.

Analyzing the trend in its profitability, Coherent’s adjusted operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q3, Coherent generated an adjusted operating margin profit margin of 19.5%, up 3.4 percentage points year on year. This increase was a welcome development and shows it was more efficient.

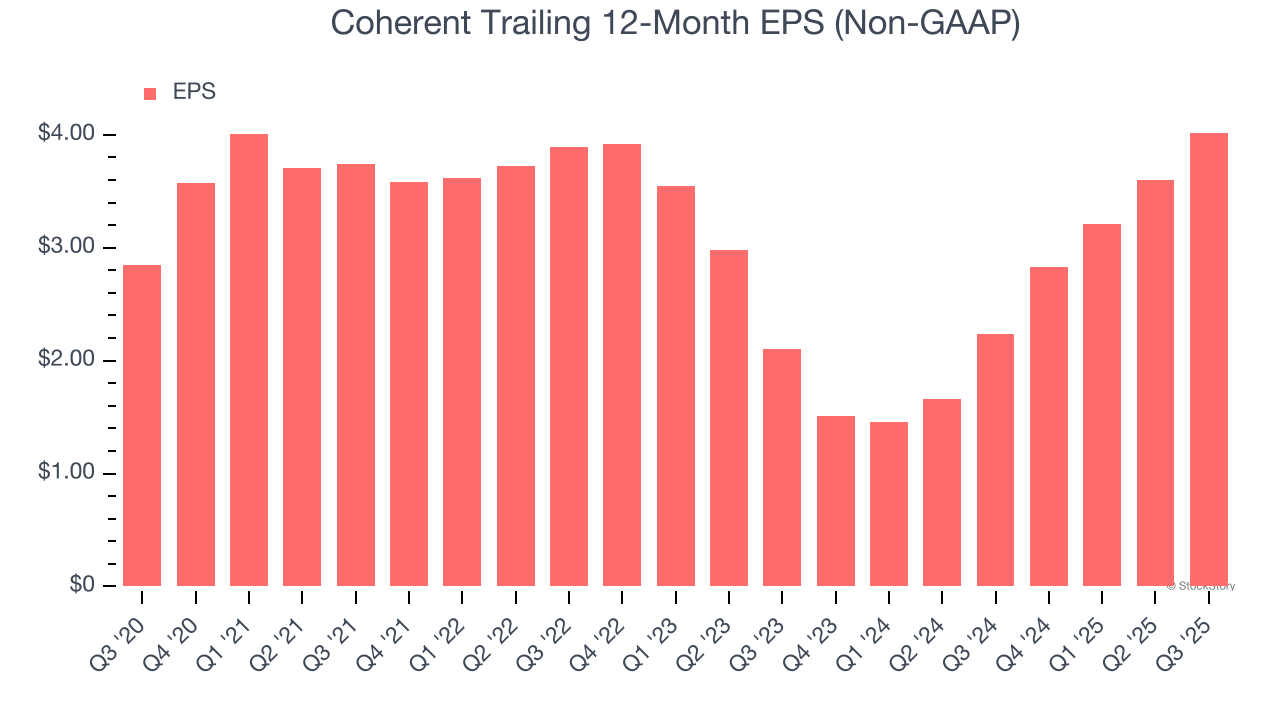

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Coherent’s EPS grew at an unimpressive 7.1% compounded annual growth rate over the last five years, lower than its 16.9% annualized revenue growth. However, its adjusted operating margin didn’t change during this time, telling us that non-fundamental factors such as interest and taxes affected its ultimate earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Coherent, its two-year annual EPS growth of 38.4% was higher than its five-year trend. This acceleration made it one of the faster-growing business services companies in recent history.

In Q3, Coherent reported adjusted EPS of $1.16, up from $0.74 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Coherent’s full-year EPS of $4.02 to grow 22.1%.

Key Takeaways from Coherent’s Q3 Results

We were impressed by how significantly Coherent blew past analysts’ EPS guidance for next quarter expectations this quarter. We were also glad its revenue guidance for next quarter trumped Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 5.9% to $142.61 immediately after reporting.

Sure, Coherent had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.