The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how professional tools and equipment stocks fared in Q3, starting with Lincoln Electric (NASDAQ: LECO).

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand. Some professional tools and equipment companies also provide software to accompany measurement or automated machinery, adding a stream of recurring revenues to their businesses. On the other hand, professional tools and equipment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 9 professional tools and equipment stocks we track reported a strong Q3. As a group, revenues beat analysts’ consensus estimates by 2.1% while next quarter’s revenue guidance was in line.

While some professional tools and equipment stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 1.7% since the latest earnings results.

Lincoln Electric (NASDAQ: LECO)

Headquartered in Ohio, Lincoln Electric (NASDAQ: LECO) manufactures and sells welding equipment for various industries.

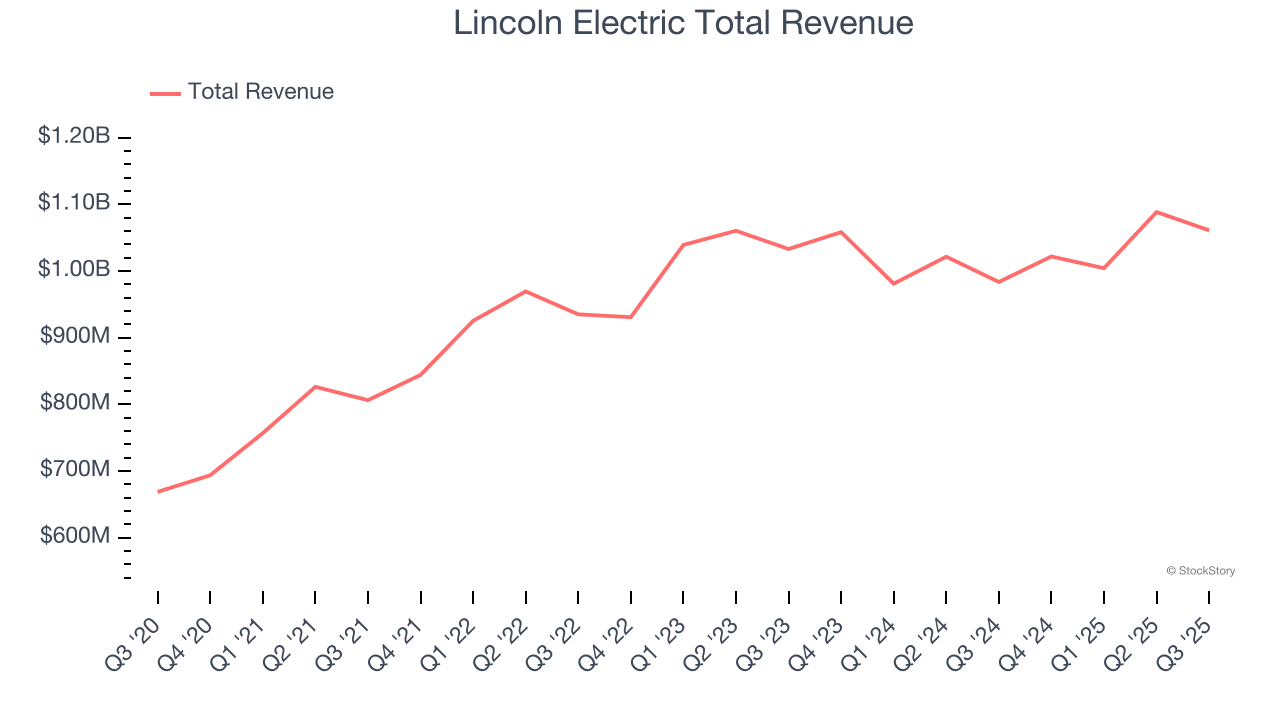

Lincoln Electric reported revenues of $1.06 billion, up 7.9% year on year. This print exceeded analysts’ expectations by 1.6%. Overall, it was a satisfactory quarter for the company with an impressive beat of analysts’ organic revenue estimates but a slight miss of analysts’ EBITDA estimates.

"We achieved strong quarterly results with an increase in profit margins, solid adjusted earnings growth, and record cash flow generation,” said Steven B. Hedlund, Chairman and Chief Executive Officer.

Unsurprisingly, the stock is down 1.1% since reporting and currently trades at $232.00.

Is now the time to buy Lincoln Electric? Access our full analysis of the earnings results here, it’s free for active Edge members.

Best Q3: Kennametal (NYSE: KMT)

Involved in manufacturing hard tips of anti-tank projectiles in World War II, Kennametal (NYSE: KMT) is a provider of industrial materials and tools for various sectors.

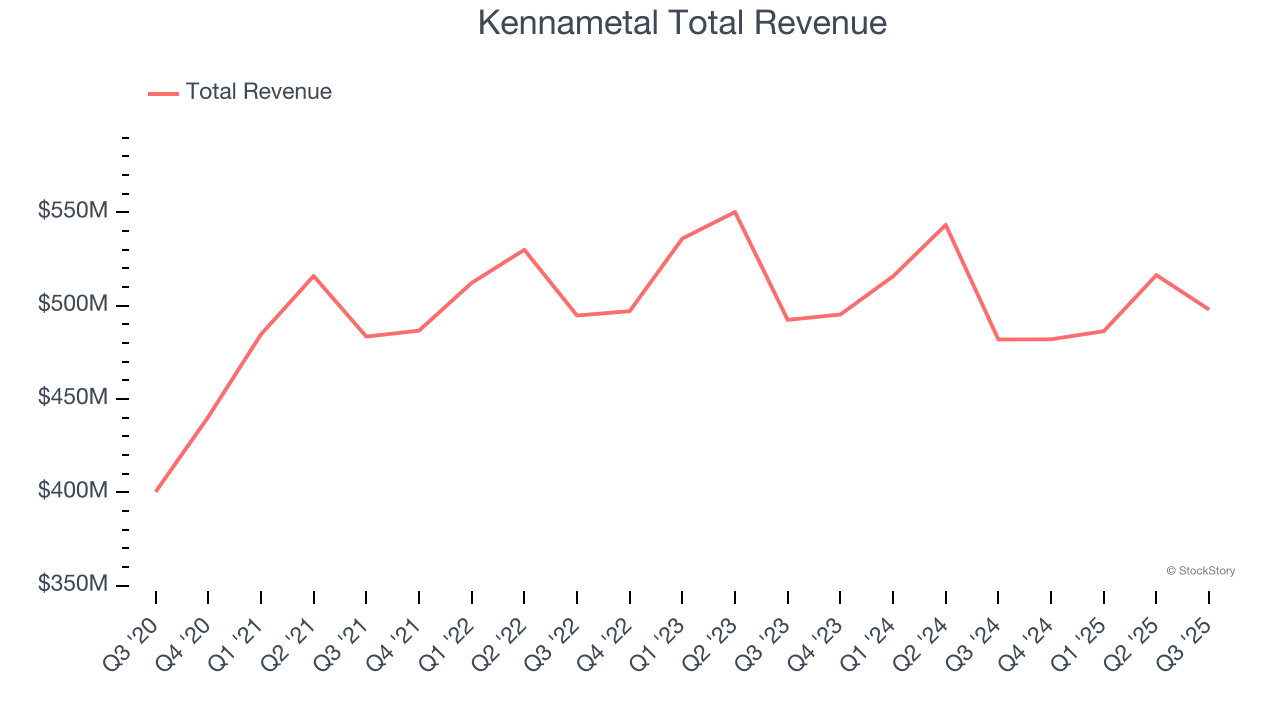

Kennametal reported revenues of $498 million, up 3.3% year on year, outperforming analysts’ expectations by 4.3%. The business had an incredible quarter with an impressive beat of analysts’ organic revenue estimates and EPS guidance for next quarter exceeding analysts’ expectations.

Kennametal achieved the highest full-year guidance raise among its peers. The market seems happy with the results as the stock is up 22.7% since reporting. It currently trades at $27.12.

Is now the time to buy Kennametal? Access our full analysis of the earnings results here, it’s free for active Edge members.

Slowest Q3: Stanley Black & Decker (NYSE: SWK)

With an iconic “STANLEY” logo which has remained virtually unchanged for over a century, Stanley Black & Decker (NYSE: SWK) is a manufacturer primarily catering to the tool and outdoor equipment industry.

Stanley Black & Decker reported revenues of $3.76 billion, flat year on year, in line with analysts’ expectations. It was a mixed quarter as it posted a beat of analysts’ EPS estimates but full-year EPS guidance slightly missing analysts’ expectations.

Stanley Black & Decker delivered the weakest performance against analyst estimates in the group. Interestingly, the stock is up 1.7% since the results and currently trades at $67.46.

Read our full analysis of Stanley Black & Decker’s results here.

Hyster-Yale Materials Handling (NYSE: HY)

Playing a significant role in the development of the hydraulic lift truck, Hyster-Yale (NYSE: HY) designs, manufactures, and sells materials handling equipment to various sectors.

Hyster-Yale Materials Handling reported revenues of $979.1 million, down 3.6% year on year. This print beat analysts’ expectations by 2.5%. It was a strong quarter as it also produced a beat of analysts’ EPS estimates and a solid beat of analysts’ revenue estimates.

Hyster-Yale Materials Handling had the slowest revenue growth among its peers. The stock is down 18.1% since reporting and currently trades at $28.36.

Middleby (NASDAQ: MIDD)

Holding a Guinness World Record for creating the world’s fastest conveyor pizza oven, Middleby (NYSE: MIDD) is a food service and equipment manufacturer.

Middleby reported revenues of $982.1 million, up 4.2% year on year. This number topped analysts’ expectations by 2.2%. Overall, it was a strong quarter as it also put up a solid beat of analysts’ revenue estimates and a beat of analysts’ EPS estimates.

The stock is down 6.3% since reporting and currently trades at $115.71.

Read our full, actionable report on Middleby here, it’s free for active Edge members.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.