Not so long ago, Palantir Technologies (PLTR) was one of the hottest artificial intelligence (AI) and analytics stocks on Wall Street. Investors loved the company’s story, using generative AI to grow its commercial business while also landing big government contracts. That powerful combination helped the stock stage a massive rally and become a clear favorite in the AI space. But 2026 has introduced a sharp shift in sentiment.

Shares of Palantir have pulled back into double-digit losses year-to-date (YTD), as rising competition, particularly from AI startup Anthropic, has rattled confidence across the broader software sector. Investors are beginning to question whether Palantir’s business model can maintain its edge in an increasingly crowded and rapidly evolving AI landscape, triggering a wave of selling pressure on Wall Street. Still, the bearish narrative isn’t going unchallenged.

In fact, analysts at Wedbush argue that the recent pullback reflects sector-wide anxiety rather than any fundamental weakness in Palantir’s business. They highlight that while Anthropic’s explosive growth has captured headlines, it is not coming at Palantir’s expense. Instead, Palantir continues to fire on all cylinders, with U.S. commercial revenue surging 137% year-over-year (YOY) and government business accelerating 66%, clear evidence that demand for its platforms remains robust.

Moreover, according to Wedbush, Palantir is still right at the center of the AI boom, with a strong data moat thanks to its Artificial Intelligence Platform (AIP) and unique way of organizing data. The firm believes this trench remains intact and is not being disrupted by tools like Anthropic’s Claude. If anything, the growing adoption of AI across enterprises is further strengthening Palantir’s position.

Keeping all these factors in mind, Wedbush remains firmly bullish, reiterating its “Outperform” rating and setting a lofty $230 price target. Given this bullish argument from Wedbush, let’s take a closer look at Palantir stock.

About Palantir Stock

Few companies have captured Wall Street’s attention in the AI era quite like Palantir Technologies. Founded in 2003 with a bold mission to help organizations make sense of massive, complex data, the Denver-based company has built powerful platforms like Gotham, Foundry, and its newer Artificial Intelligence Platform (AIP), launched in early 2023. These tools help governments and businesses analyze data, spot patterns, and make faster, smarter decisions.

Palantir first rose to prominence through its deep ties with intelligence agencies and the U.S. military, where its software played a key role in counterterrorism and national security efforts. Over time, it successfully expanded into the commercial world, helping companies across industries like healthcare, manufacturing, energy, and finance unlock valuable insights from their data.

Palantir’s fundamentals remain hard to ignore. This comes as reports suggest the U.S. military is using Palantir’s AI-powered Maven Smart System to identify targets in the Middle East during strikes on Iran that began in late February.

Still, despite its strong positioning, 2026 hasn’t been smooth for Palantir. The stock has faced pressure amid a broader pullback in tech and software names, driven by Anthropic rolling out new Claude plugins, growing concerns about a potential AI bubble, and increasing scrutiny around high valuations.

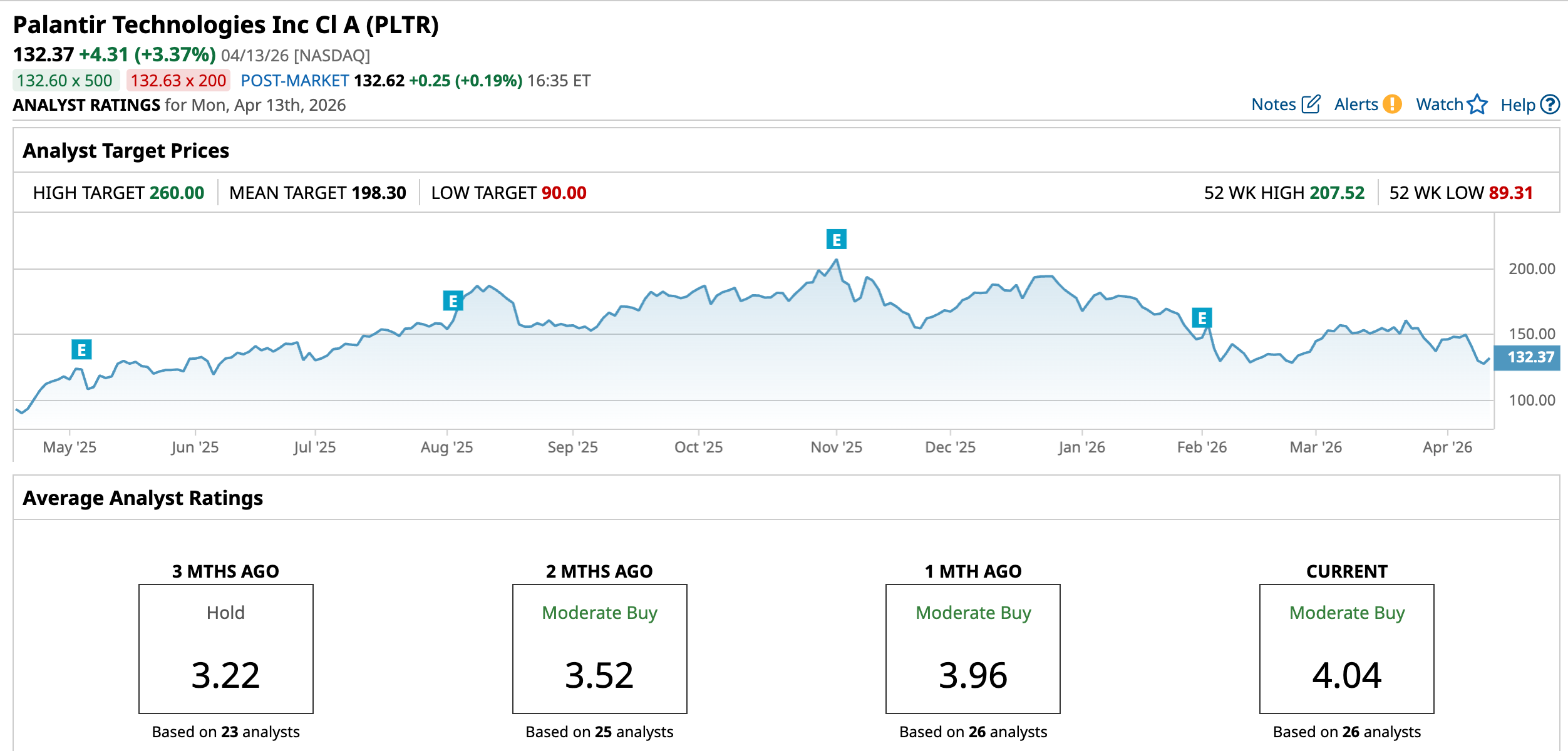

Shares are down 25.53% so far this year, sharply underperforming the S&P 500 Index ($SPX), which shows a marginial increase in 2026. After hitting a 52-week high of $207.52 in November last year, the stock has now fallen about 36.3% from that peak, marking a notable pullback for one of the market’s biggest AI names. The company’s market capitalization currently stands at roughly $306.3 billion.

Valuation continues to be a key concern for Palantir. Even after a major pullback so far in 2026, the stock still trades at steep premiums, with a lofty 127.9 times forward earnings and 67.80 times sales (TTM). These levels make it clear that investors have already priced in significant future growth. In contrast, the broader sector trades at much lower multiples of about 21.6 times forward earnings and 3.1 times sales, highlighting just how expensive Palantir remains relative to its peers.

Inside Palantir’s Q4 Earnings Results

When Palantir unveiled its fiscal 2025 fourth-quarter results in early February, it underscored exactly why the company continues to command attention in the AI space. The data analytics firm wrapped up the year with record-setting performance, delivering the strongest quarterly results in its 23-year history. Revenue reached roughly $1.41 billion, the highest ever for a single quarter.

This marked a sharp 70% YOY jump and came in well ahead of Wall Street’s $1.34 billion estimate. Growth was largely driven by the U.S. market, which now makes up about 77% of total revenue. Within that, the U.S. Commercial segment stood out as the primary growth driver, with revenue surging 137% YOY to $507 million, powered by strong enterprise demand for its Artificial Intelligence Platform (AIP).

Meanwhile, Palantir’s government business also remained a key contributor. U.S. government revenue totaled $570 million, up 66% from a year ago. Strong deal activity further reflected rising demand, with the company closing 180 deals worth at least $1 million, including 84 deals above $5 million and 61 deals exceeding $10 million during the quarter.

Total contract value (TCV) hit a record $4.262 billion, representing a 138% YOY increase. Of this, U.S. commercial TCV reached a new high of $1.344 billion, up 67% compared to last year. On the profitability front, the company delivered equally strong results. Palantir reported GAAP net income of $609 million, translating to a 43% margin and an impressive 670% YOY increase. Adjusted earnings per share came in at $0.25, ahead of the Street’s $0.23 estimate.

Also, the company ended the year in a strong financial position, with $7.2 billion in cash and short-term securities, providing ample room for continued investment in innovation and large-scale sovereign AI initiatives.

Looking ahead, management struck a confident tone for fiscal 2026. The company expects full-year revenue to fall between $7.182 billion and $7.198 billion, implying around 61% growth. Even more notable, U.S. commercial revenue is projected to surpass $3.144 billion, indicating at least 115% growth, signaling that enterprise adoption of its AI platform could remain a major driver in the year ahead.

How Are Analysts Viewing Palantir Stock?

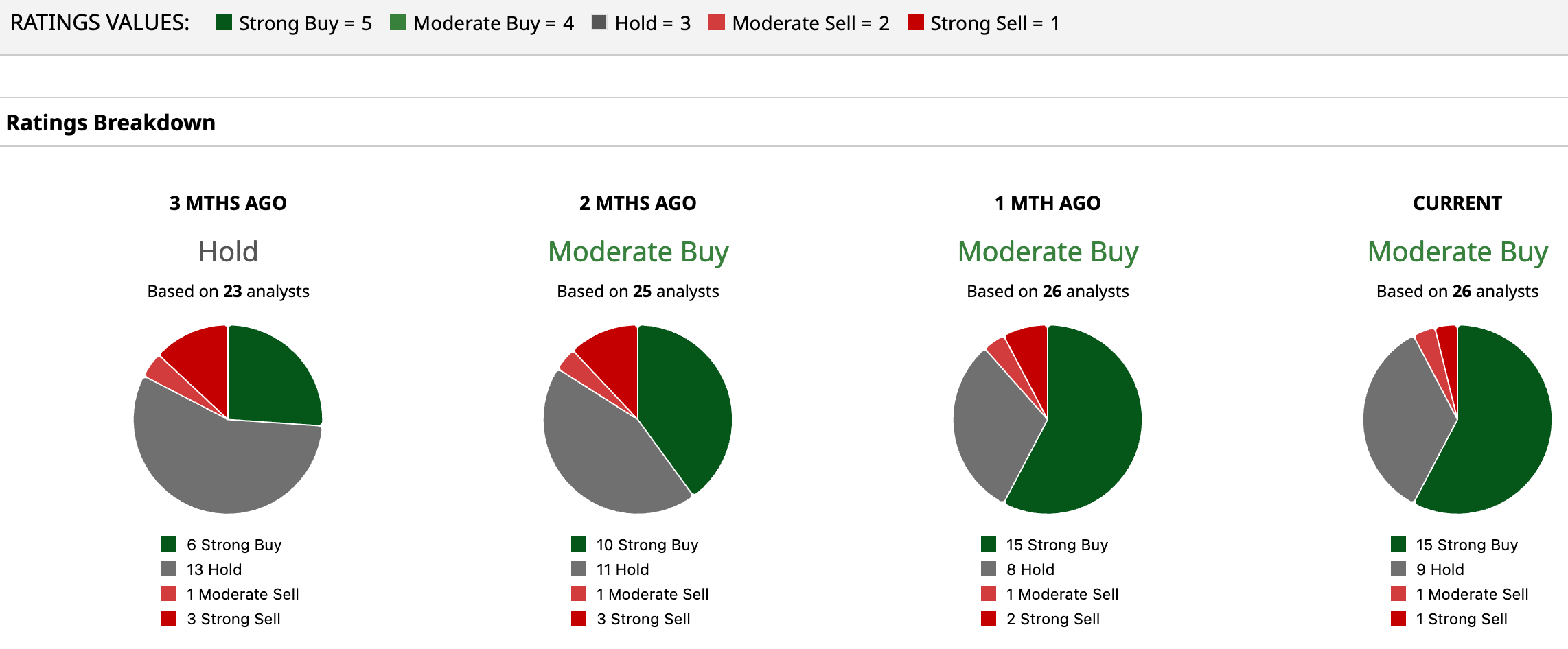

Despite the recent swings in Palantir shares, Wall Street hasn’t lost confidence. The stock still carries a consensus “Moderate Buy” rating, showing that most analysts remain optimistic about its outlook. Of the 26 analysts covering the name, 15 are firmly bullish with “Strong Buy” ratings, while nine prefer to stay cautious with “Hold.” Only two analysts lean bearish, with one “Moderate Sell” and one “Strong Sell,” making it clear that negative sentiment is still very limited.

The upside potential in Palantir still looks compelling. The average price target of $198.30 suggests a solid 49.8% upside from current levels, while the Street-high target of $260 points to a potential surge of 96.4%, showing just how bullish some analysts remain on the stock’s future.

On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart