Cloud communication provider RingCentral (RNG) experienced a significant surge after reporting its fourth-quarter results, with its stock gaining 34.4% intraday on Feb. 20. The company has gained considerable momentum due to its artificial intelligence (AI) offerings. This year, RingCentral’s stock is up nearly 40% after a slump last year.

The company reported that its annual recurring revenue (ARR) from customers using the tools doubled annually to nearly 10%. RingCentral also recently integrated ChatGPT models into its voice AI offerings, ushering in a new phase of enterprise voice intelligence powered by OpenAI. Such tailwinds have led RingCentral to issue an optimistic outlook for the current year, even surpassing Street analysts’ consensus estimate.

Are there more upsides left in the stock?

About RingCentral Stock

Based in Belmont, California, RingCentral excels in delivering cloud communications platforms to global businesses. Its unified system combines voice calls, video meetings, messaging, fax, and contact center tools via a robust, secure cloud network spanning regions. Emphasizing AI enhancements for intelligent conversations, automation, and team productivity, it powers flexible hybrid workplaces.

Mobile-friendly options like texting, virtual conferences, and app integrations modernize operations, ditching legacy hardware phones. RingCentral prioritizes scalability, data protection, and cutting-edge features to boost engagement for customers and staff in diverse sectors. The company has a market capitalization of $3.42 billion.

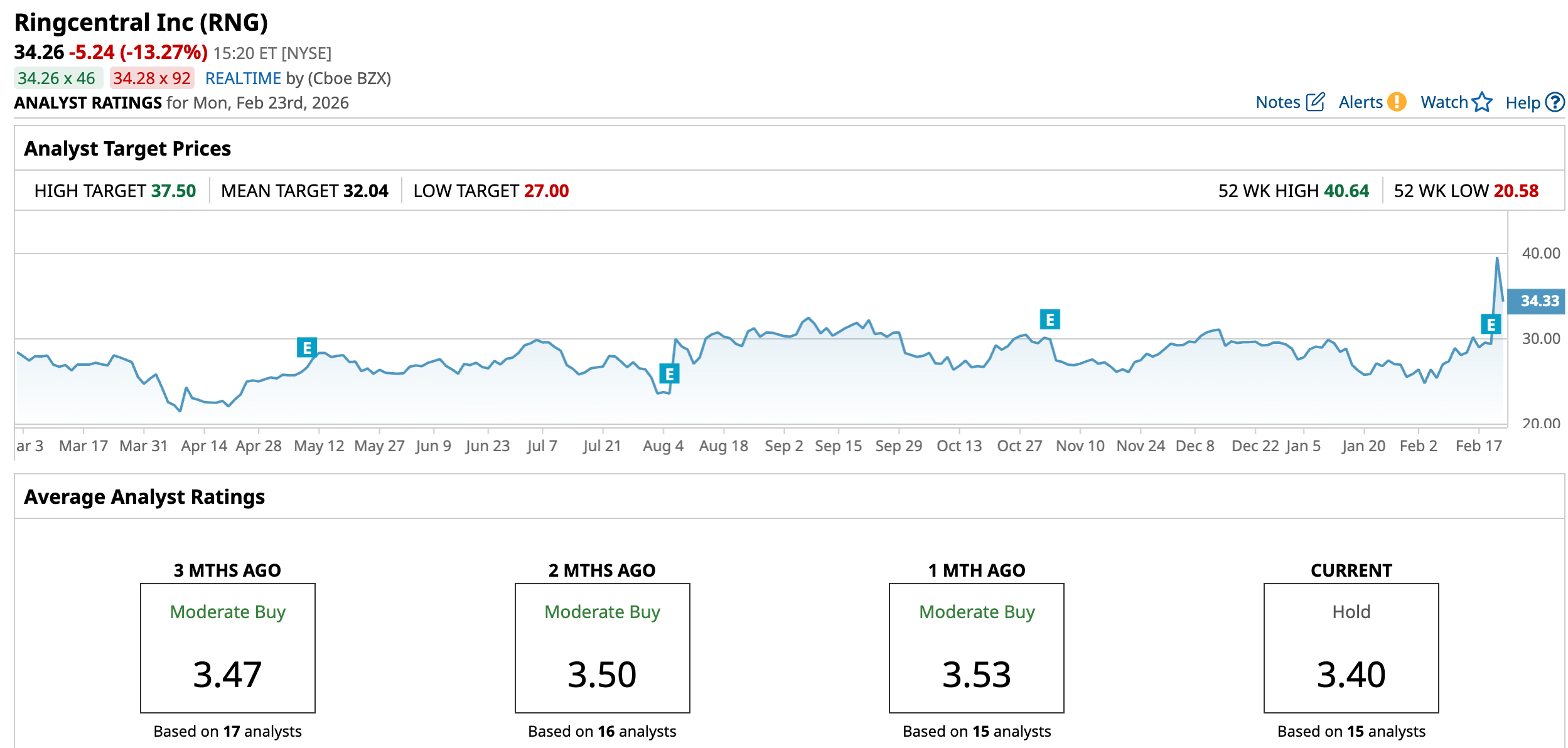

RingCentral’s stock has benefited from the company’s AI products. Its cash generation abilities, as evidenced by its new dividend, have also kept the stock buoyant. Over the past 52 weeks, it has gained 18.55%, and it is up 18.84% year-to-date (YTD). Just for comparison, the broader S&P 500 Index ($SPX) has gained 13.64% over the past 52 weeks and marginally down 0.18% YTD. The stock reached a 52-week high of $40.64 on Feb. 20, but is down 18% from that level.

On a forward-adjusted basis, RingCentral’s price-to-earnings ratio of 8.16x is lower than the industry average of 22.65x.

RingCentral Delivers Strong Q4 Results with Margin Expansion and Solid Cash Flow

On Feb. 19, RingCentral reported better-than-expected fourth-quarter results for fiscal 2025, leading to a massive surge in the stock on Feb. 20. The company’s total revenue increased 4.8% year-over-year (YOY) to $644.03 million, which was higher than the $642.30 million that Wall Street analysts had expected. This was based on subscription revenue increasing by 5.5% YOY to $622.22 million.

RingCentral’s new AI-led products generated $100 million in ARR, with AI Receptionist (AIR) now serving more than 8,000 customers, up 44% sequentially.

Based on the top line growth, the company’s margins expanded robustly. Its non-GAAP operating margin increased from 21.3% to 22.8% YOY, while non-GAAP free cash flow rose 12.8% from the prior-year period to $126.13 million. The company’s non-GAAP EPS was $1.18, up 20.4% YOY and higher than the $1.14 that analysts had expected.

Wall Street analysts have a robustly positive view about RingCentral’s bottom line trajectory. For the current quarter, its EPS is expected to increase 74.1% YOY to $0.47. For the current fiscal year, EPS is expected to grow by 23.3% to $2.49. Moreover, for the next fiscal year, the company’s EPS is projected to increase by 20.1% annually to $2.99.

What do Analysts Think About RingCentral’s Stock?

Post the Q4 earnings, Rosenblatt analyst Catharine Trebnick maintained a bullish “Buy” rating on RingCentral’s stock, while raising the price target from $32 to a Street-high of $37.50. Trebnick sees further prospects after the company’s “solid” results, and its strong outlook and free cash flow “underscores a durable profitable growth profile.”

However, other analysts have a more tepid view of RingCentral. After its results, analysts at Mizuho maintained a “Neutral” rating on the stock, but raised the price target from $27 to $32. Mizuho analysts noted that RingCentral is evolving its financial framework to better align with its current growth trajectory, while advancing innovation and rolling out new products. Last month, Morgan Stanley's analyst Elizabeth Porter maintained an “Equal Weight” rating on the stock, but lowered the price target from $31 to $30.

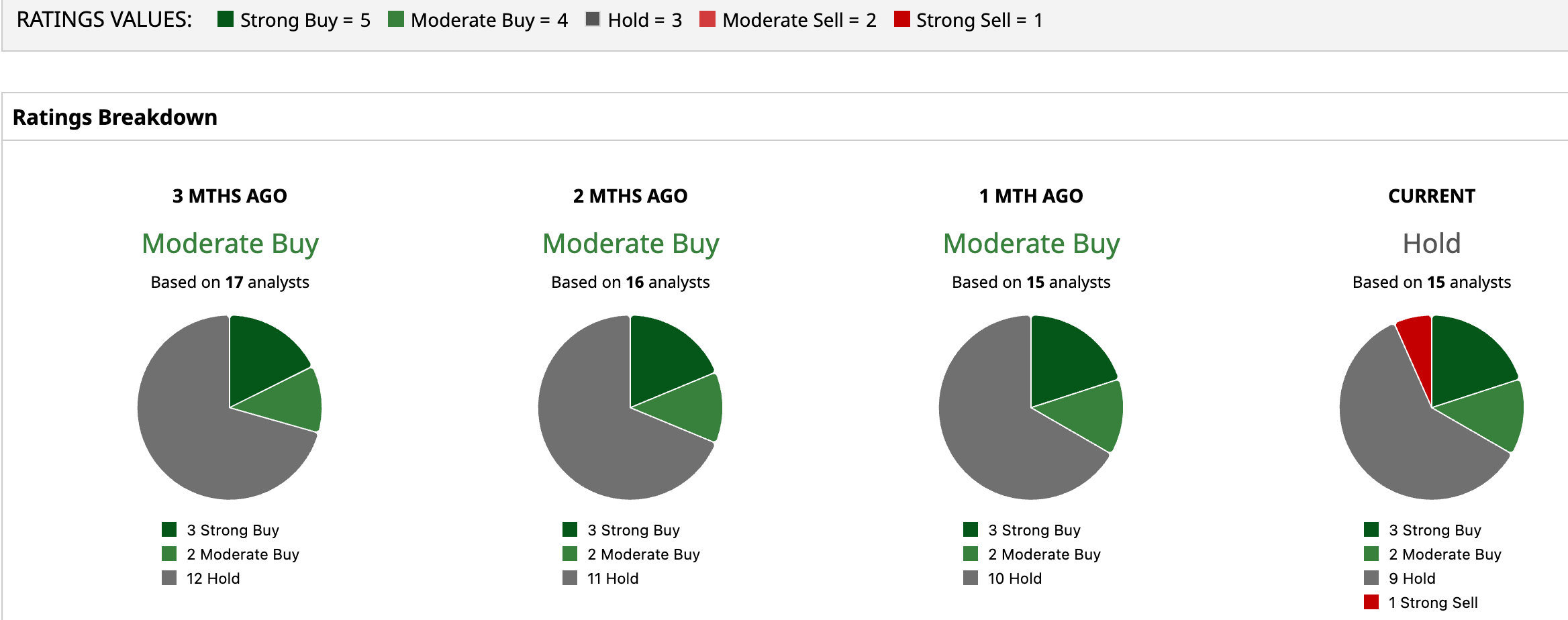

Wall Street analysts are taking a cautious stance on RingCentral’s stock now, with a consensus “Hold” rating overall. Of the 15 analysts rating the stock, three analysts gave a “Strong Buy” rating, two analysts gave a “Moderate Buy” rating, while a majority of nine analysts are playing it safe with a “Hold” rating, and one analyst gave a “Strong Sell” rating. The current price sits above the consensus price target of $32.04, and the Street-high Rosenblatt-given price target of $37.50 indicates 9.5% growth from current levels.

On the date of publication, Anushka Dutta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Novo Nordisk Stock Is Deeply Oversold on Weight Loss Drug Fail. Should You Buy the Dip?

- Should You Buy Dell Stock Before February 26? This Analyst Says Yes.

- Everything You Need to Know About Musk’s ‘Self-Growing’ Moon City as He Races to ‘Secure the Future of Civilization’

- PayPal Has Attracted Takeover Interest. Does That Make PYPL Stock a Buy Here?