The Justice Department has launched a formal antitrust investigation into Netflix’s (NFLX) proposed $83 billion acquisition of Warner Bros. Discovery’s (WBD) core assets, including its film and television studios, HBO, and HBO Max streaming service. Regulators are closely examining whether the transaction would substantially lessen competition in the streaming and entertainment industries or allow Netflix to exert undue influence over independent creators through its dominant negotiating power.

Citing potential breaches of Section 7 of the Clayton Act and Section 2 of the Sherman Act, the probe goes beyond standard merger review to assess broader monopolization risks. The deal—already unpopular with investors—has driven NFLX shares sharply lower, and the antitrust scrutiny now stands as a potential wedge that could knock Netflix out of contention entirely, especially as rival Paramount Skydance (PSKY) just cleared a DOJ review of its own.

Netflix Stock Bears Brunt of Investor Dissatisfaction

NFLX shares have borne the full weight of investor unease in 2026, falling 20% year-to-date and an additional 22% since the Warner Bros. Discovery deal was announced. That performance badly lags the S&P 500 ($SPX), which has managed a modest 0.3% gain over the same period. At a forward price-to-sales multiple of approximately 7.2, the stock trades at a noticeable premium to the movies-and-entertainment industry average of roughly 3.5. Yet it sits comfortably below Netflix’s own historical average P/S of about 8.1.

The forward P/S reflects expectations of solid top-line growth but also embeds skepticism about the deal’s financing, integration costs, and regulatory overhang. A lower-than-historical multiple suggests the market is pricing in meaningful risk that the acquisition could destroy rather than create value, while the premium to peers underscores Netflix’s still-superior growth profile and profitability.

Taken together, the valuation appears fairly valued at best for a standalone streaming leader, but the post-announcement selloff signals that many investors see the Warner Bros. transaction as an expensive distraction rather than a strategic masterstroke.

Why Netflix Investors Should Welcome the Antitrust Review

Far from a purely negative development, the DOJ’s sweeping antitrust inquiry gives Netflix shareholders a compelling reason for relief. The $83 billion asset purchase would saddle the balance sheet with significant new debt—Warner Bros. Discovery already carries heavy obligations—while exposing Netflix to integration headaches in an increasingly fragmented content landscape. Many investors have openly questioned the premium being paid and the strategic logic of blending two large streaming services when organic growth and advertising-tier expansion already deliver strong returns.

The investigation itself is unusually broad. Civil investigative demands have gone out to filmmakers and producers, requiring detailed document production and sworn testimony by March 23. Investigators are zeroing in on Netflix’s historical leverage in content negotiations and whether the merger would further entrench that power, potentially violating both merger-specific statutes and longstanding monopolization prohibitions. Sources close to the Trump administration describe the review as extending well beyond Hart-Scott-Rodino formality into a full assessment of competitive harm.

Meanwhile, Paramount Skydance continues pressing its competing all-company offer, recently signaling a willingness to raise its bid to as high as $33 per share and claiming its proposal has already cleared a key HSR waiting period. Warner Bros. Discovery shareholders are slated to vote on the Netflix deal on March 20, but the DOJ timeline could easily push that date or kill the transaction outright.

Political undercurrents—Netflix board member Susan Rice’s past criticism of President Trump, Republican wariness of the streamer’s content, and Democratic concerns over lobbying—only intensify the spotlight.

For long-term shareholders, a blocked or delayed deal preserves capital discipline, avoids dilution risks, and lets management double down on what has worked: subscriber momentum, ad-tier rollout, and original content leadership. The antitrust process, while creating near-term uncertainty, ultimately acts as a market-friendly circuit breaker against a transaction many viewed as overreaching.

What Do Analysts Expect for NFLX Stock?

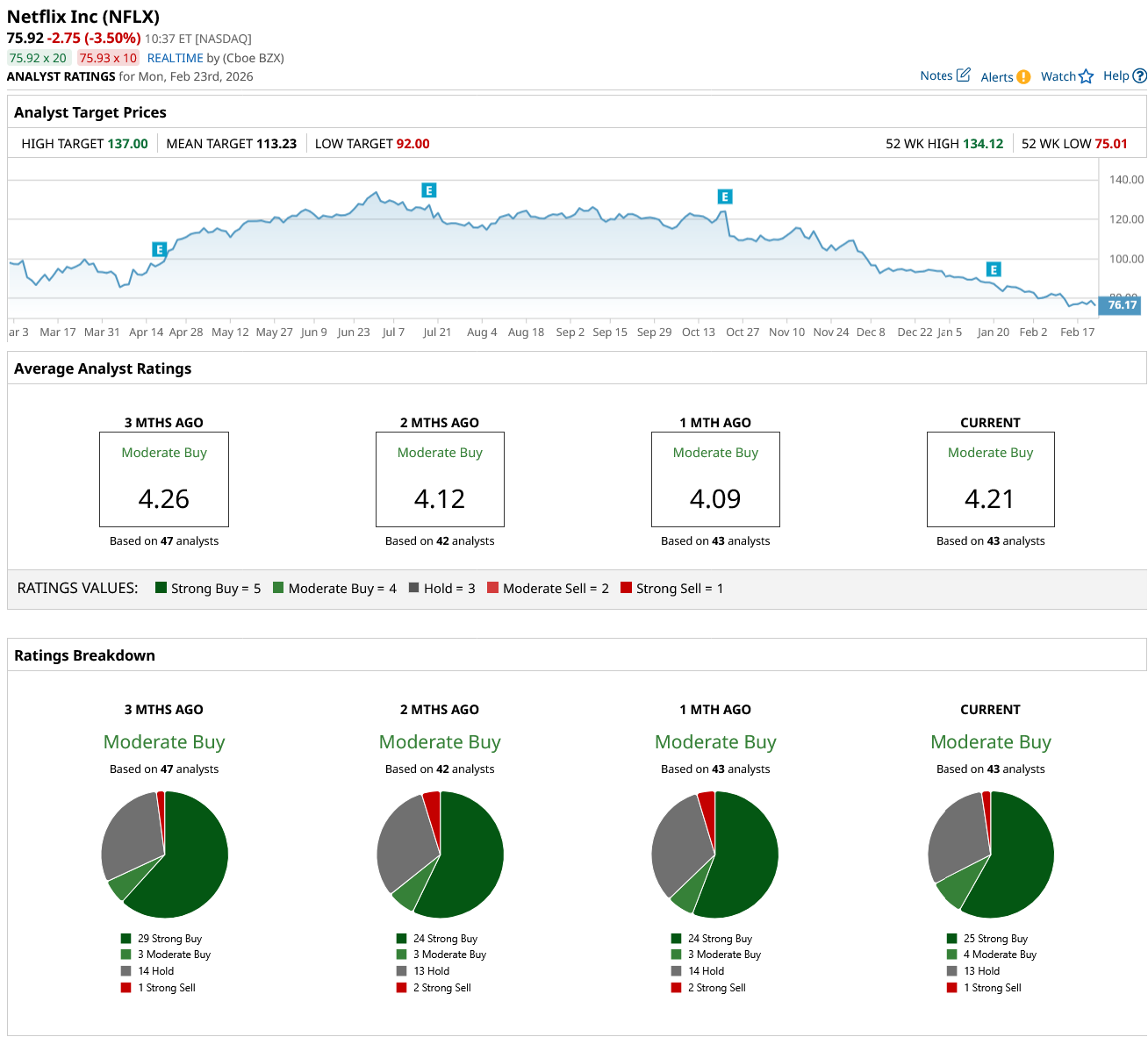

Wall Street analysts continue to back Netflix even as the merger drama unfolds. Barchart’s consensus rating stands at "Moderate Buy," drawn from 43 analysts covering the name. The ratings breakdown shows 25 "Strong Buy" ratings, four "Moderate Buy" ratings, 13 "Hold," and one "Strong Sell." Opinion has remained remarkably stable in recent months, with a modest softening that has not altered the overall bullish tilt.

Analysts' mean price target is $113.23, representing a potential upside of 44%. That implied gain reflects expectations that, whether the Warner deal collapses or is restructured under regulatory pressure, Netflix’s core business—booming engagement, improving margins, and global scale—will drive a meaningful re-rating. With NFLX stock already reflecting deal fatigue, analysts see limited downside and substantial rebound potential once the antitrust overhang clears.

On the date of publication, Rich Duprey did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart