With a market cap of $15.2 billion, Avery Dennison Corporation (AVY) is a global materials science and manufacturing company specializing in pressure-sensitive labeling, packaging materials, and functional materials used across consumer goods, retail, logistics, and industrial markets. Founded in 1935 and headquartered in Mentor, Ohio, the company supplies branding and information solutions that help customers identify, track, and protect products throughout the supply chain.

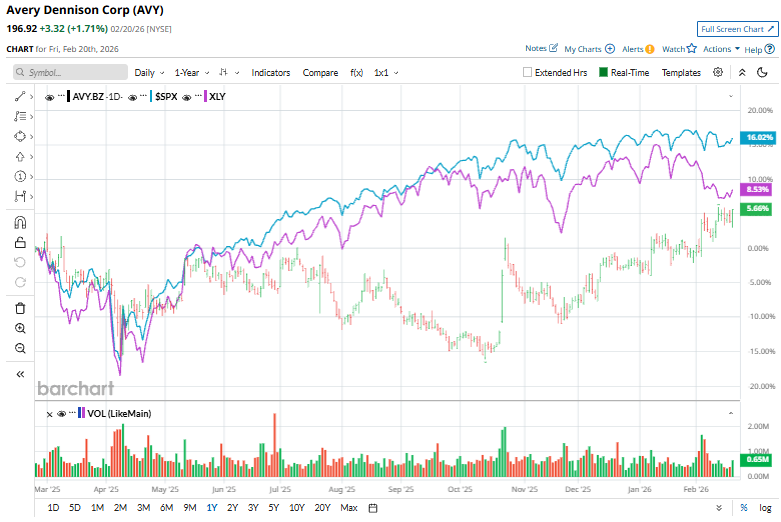

Avery Dennison has substantially underperformed the broader market over the past year. AVY stock prices have soared 6.9%, compared to the S&P 500 Index’s ($SPX) 13% gains. However, in 2026, the stock has surged 8.3%, surpassing SPX’s marginal rise.

Taking a closer look, AVY has also underperformed the State Street Consumer Discretionary Select Sector SPDR Fund’s (XLY) 4.7% uptick over the past year but has outpaced its 1.6% year-to-date dip.

On Feb. 4, Avery shares popped 3.4% after the company released its fiscal 2025 fourth-quarter earnings. Revenue rose 3.9% year over year to $2.27 billion, slightly below expectations, while adjusted EPS of $2.45 increased 3% and topped estimates. Additionally, operating margins compressed year over year as deflation-related pricing and tariff headwinds offset low-single-digit volume gains, particularly in Materials.

For the current year ending in December, analysts expect AVY to deliver an adjusted EPS of $10.13, up 6.3 year over year. The company has a mixed earnings surprise history. While it missed the Street’s bottom-line estimates once over the past four quarters, it has surpassed the projections on three other occasions.

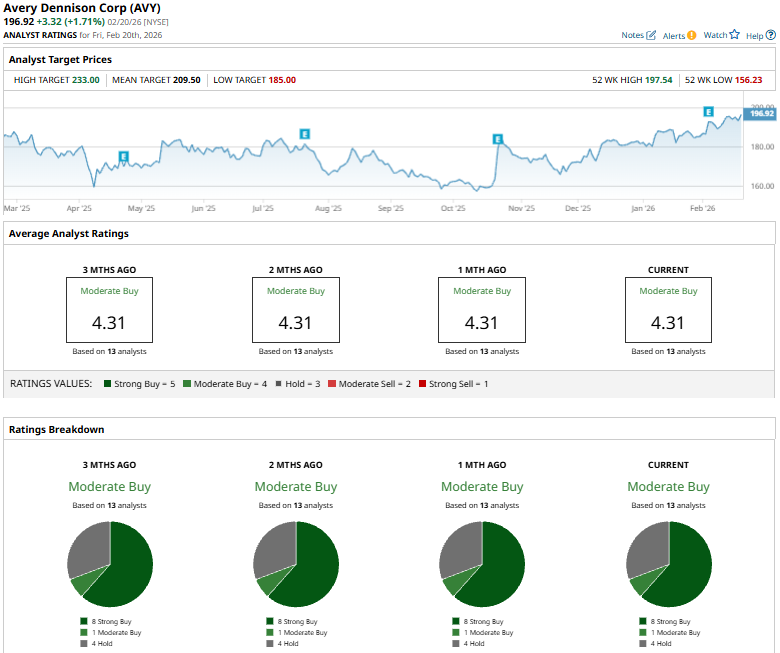

Among the 13 analysts covering the AVY stock, the consensus rating is a “Moderate Buy.” That’s based on eight “Strong Buys,” one “Moderate Buy,” and four “Holds.”

On Feb. 10, JPMorgan analyst Jeffrey Zekauskas reiterated an “Overweight” rating on Avery Dennison and raised the price target to $205 from $195, signaling continued confidence in the company’s outlook.

While AVY’s mean price target of $209.50 represents a 6.4% premium to current price levels, the street-high target of $233 suggests a notable 18.3% upside potential.

On the date of publication, Kritika Sarmah did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Nvidia May Have Dumped Arm Stock in Q4, But Should You Buy Shares Now?

- 3 New Stocks Billionaire Dan Loeb Is Betting on Now

- This Penny Stock Is Building a Strategic Silver Reserve. Should You Buy Shares Now to Bet on a Run in Silver Prices?

- 3 Stocks Warren Buffett and Berkshire Were Gobbling Up in Q4